Emerging Self Storage Hot Spots: New England Joins the West and Midwest in Offering the Greatest Growth Opportunities

Share this article:

- New England, western and midwestern metro areas can most benefit from the addition of new self storage space due to a combination of low inventories and robust interest in storage away from home.

- Springfield, MA, stands out with the biggest gap between supply and demand. While there’s only 3.7 square feet of space per person, the city’s population has jumped by 10.8% in the last 10 years. With high housing density and small apartments, the squeeze is definitely on.

- Seven of the top 10 underserved cities for self storage are tertiary markets.

- Among the primary markets, the Phoenix, Los Angeles, and Philadelphia metro areas still show promise for new self storage development.

The self storage industry has seen unprecedented growth lately, with the past 10 years delivering an impressive 25% of the total existing inventory of self storage nationwide. Although still below prepandemic levels in terms of new supply, 2023 has seen a robust 53M square feet of new space added to the market, and 2024 is on track to see the delivery of no less than 54M rentable square feet.

Demand is at the core of the sustained development pace in the self storage market, traditionally driven by the four D’s: death, divorce, dislocation and downsizing. These factors have long been fundamental to the interest in self storage, leading to one-fifth of Americans relying on storage away from home to maximize space.

Recently, two more D’s — decluttering and distribution — have become significant drivers, rounding out what are now the six D’s of self storage. The shift toward working from home (WFH) — whether fully remote or hybrid — and the shrinking home sizes have created a need for people to declutter more than in the past. Additionally, the boom in e-commerce has prompted small businesses to seek efficient distribution solutions. In this context, self storage has emerged as a viable alternative to traditional warehouse space. It is often more affordable and offers greater flexibility, with lower rates and extensive geographic coverage. Moreover, the intensifying popularity of RV-ing, along with the resurgence of snowbirding after the pandemic lows, has given a strong boost to vehicle storage, creating a new and expanded clientele for self storage businesses.

Since the market’s success often boils down to a game of supply and demand, we decided to take a closer look at how different areas are keeping up with current self storage needs. Our RentCafe storage research team scoped out the largest 150 U.S. metro areas to pinpoint where there is still untapped potential for self storage development and where — on the opposite end — the market is well positioned to meet existing demand. We based our analysis on a set of 25 criteria including:

- The local self storage inventory per capita, calculated as availability of storage space within a three-to-five-mile radius

- Interest in self storage services as expressed by storage-related online searches

- Demographic factors of demand including population growth, household size and household formation

- Urbanization and housing based on the number of building permits in a specific location, average apartment size, percentage of apartments with storage, rental competitivity and for-sale market evolution

- Household car ownership rates and local demand for car storage services by also taking into account local vehicle storage stock

- The population of college students and their interest in storage solutions

- Number of remote workers and the associated demand for home organization

- Economic factors, such as income growth, household income, employment-related data and more

So where are the next chapters of self storage development most likely to unfold? It looks like it’s the tertiary markets’ time to shine. Our ranking of the most promising self storage markets where the industry has room to grow — essentially the places where demand meets limited supply — is dominated by smaller metropolitan areas with populations under 2 million.

Supply is in fact generally lower in tertiary markets, as developers have traditionally chased population flows into the big urban centers. However, with recent shifts in migration patterns and growth spiking in smaller markets, demand for extra space is also flourishing in new places. Of course there are other factors at play aside from migration. Trends toward smaller home spaces and minimalism, along with tight housing markets, often lead to an increased demand for storage. High move-in activity, more common in cities with large renter populations and college towns, contributes too, as does the resurgence of multigenerational living. Moreover, strong business and economic landscapes are increasingly driving demand in the storage market.

Key underserved markets: With low inventories and strong interest for self storage, New England metros are primed for growth

The blend of economic strength, dense housing markets and an abundance of lifestyle options is a boon for self storage businesses — and it’s this combination that’s putting smaller cities in New England and the Midwest on the map for self storage opportunities.

Boasting several potential sources of demand, New England is worth keeping an eye on. Springfield, MA, ranks first nationally as a self storage opportunity zone. It has the country’s second-lowest self storage inventory per capita, at 3.7 square feet, just half of the national benchmark. With a 10-year population increase of 10.8%, positive migration, small homes and a robust interest in self storage — over 755 Google searches related to the industry per 10,000 residents — Springfield checks multiple marks for pent-up self storage demand. The average apartment size in Springfield sits at a modest 740 square feet, the second smallest nationally. The area also hosts over 66K college students, piling on extra self storage demand factors.

Springfield is one of the country’s most active housing markets — alongside another fellow Massachusetts metro, Worcester, also in our top 20 — and a potential influx of homebuyers can add even more pressure on the limited self storage inventory. Developers are catching on and are taking steps to improve local access to self storage, with 2024 seeing a projected 234K square feet that amount to over 16% of the total existing inventory in Springfield.

Another New England hot spot, Providence-Warwick, RI-MA, landed fourth nationally for self storage development potential. Currently registering 4.8 square feet of storage space per capita, with high housing density and relatively small apartments as well as a student population of almost 92K people, the area makes a strong case for more self storage development.

Interest in self storage is strong, reflected in over 830 storage-related Google searches per 10,000 residents. The local demographic trends also provide a solid foundation for self storage growth, with positive net migration and an increasing number of households. In fact, the metro area now has nearly 10% more households than it did a decade ago.

About 45 miles west of Boston, MA, Worcester, MA-CT, rounds out the top 20 of the country’s most auspicious metros for self storage development. It features a modest 5.4 square feet of self storage space per capita, well below industry standards. Between population growth, dense living and a strong presence of college students, it’s no wonder that people in Worcester are interested in finding additional storage solutions. The local industry is already picking up on these clues and working on adding extra inventory: The new self storage planned to be delivered this year in Worcester amounts to 15% of the entire inventory.

Boston itself is not far behind in terms of potential for further expansion with the metro area currently offering 4.7 square feet of storage space per capita. As a bustling urban center, Boston experiences high population mobility and has one of the highest housing densities in the country. Adding to the demand for more storage space, the metro area is home to over half a million remote workers, more than 350K college students, and nearly a million households that own more than one car.

Honolulu, HI, the country’s most undersupplied market, shows a strong appetite for self storage

Urban Honolulu is one of the country’s most expensive self storage markets. With the monthly rate for a unit at $277 on average, more than double the national average, the area also seems to be in dire need of additional self storage space.

Nationally, it ranks second among cities offering the best opportunities to capitalize on storage demand. With the lowest per capita inventory of the 150 largest metro areas — at just 3.2 square feet of storage space per person — and the smallest average apartment size, under 700 square feet, it stands out in the storage market.

The main driver of urban Honolulu’s economy, tourism also creates extra demand for self storage. From catering companies to sports equipment rentals, many local businesses need self storage for their gear, especially during the off-peak season. Plus, with the area’s abundant outdoor activities, residents likely own more sports-related equipment than the average American. These unique local factors are increasing the pressure on self storage facilities, which are currently struggling to meet the demand.

Population growth and outdoor lifestyles fuel development potential in the Mountain West

The Mountain West region has seen massive growth in recent years, both in terms of economy and population — and the self storage industry stands to win big from this combination.

Boulder, CO, ranking third for self storage development opportunities, currently has an inventory of 6.3 square feet of space per capita, only slightly under the national benchmark. However, demand in the area is solid, with almost 1,000 online searches for self storage services per 10,000 residents, pointing to local appetence for more inventory. Boulder’s transient population, including college students and professionals, often necessitates temporary storage solutions during moves or transitions. In fact, Boulder, home to almost 50,000 students, ranks fifth among the country’s largest 150 metros for online searches related to student storage. Moreover, Boulder, with a population of just under 330K residents, registers an impressive 58,000 remote workers, further pressing on the available storage space, both at home and away from home. On top of that, the city’s active lifestyle often means residents accumulate gear for skiing, hiking and biking, and self storage becomes essential for storing seasonal equipment and outdoor gear.

Greeley, CO, is booming in self storage interest, with over 1,000 related Google searches per 10,000 residents. Even if it already boasts a healthy 7.6 square feet of self storage space per capita, the city’s population has surged by an impressive 30% over the last decade, giving way to strong demand associated with new household formation and moving. With an average household income of $91.5K, residents of Greeley also have the means to engage in various hobbies and activities, further fueling the need for self storage. Many families store sports equipment, recreational vehicles, collectibles and other items in self storage units. Business storage demand is also growing, with Greeley ranking twelfth in Google searches for business storage among the 150 metros analyzed.

The third metro area in Colorado to make it to the best markets for storage expansion is Denver-Aurora-Lakewood. The area’s self storage inventory, at 7.3 square feet per capita, aligns with the national average. Over the past decade, Denver has experienced steady growth in population and housing — the primary drivers of self storage demand. In 2023 alone, over 20,000 new building permits for housing units were issued in the metro area, making it the fourteenth most active market in the U.S. Furthermore, with nearly 400K remote workers and about 150K college students, who often depend on self storage to optimize their living spaces, Denver presents significant opportunities for self storage developers. This is underscored by more than 950 monthly self storage related Google searches per 10,000 residents.

Another western hot spot and the first primary market to make it to the top 20 markets to watch list, is Phoenix-Mesa-Chandler, AZ. The Phoenix area is holding on to its appeal as one of the best places to move to, mainly thanks to its thriving job market and living costs that are a steal compared to other major U.S. cities. Over the last decade, the metro area has seen a 14% population surge and a 22% increase in households, putting it in prime position for further expansion in the self storage sector.

With 8.4 square feet of storage space per capita, Phoenix is ready for more. The keen interest in self storage is clear: There are roughly 1,200 monthly Google searches for storage options per 10,000 residents, not to mention consistent searches for vehicle storage solutions. Phoenix is definitely a market to watch.

Student influx and remote work boom strain Rochester’s limited self storage inventory

Rochester, NY, coming in sixth, features some typical East Coast characteristics, including dense living and relatively low self storage inventory that shape it up to be a promising market for further development.

The existing local inventory amounts to only 5.2 square feet of storage space per capita. Conversely, the service is raising a lot of interest, with around 916 self storage related Google searches per 10,000 residents. The existing self storage space is further challenged by a sizeable student population of 65,000 as well as an appreciable number of remote workers — almost 73K. As remote workers face the need of setting up home offices, many of them require self storage in order to carve out the needed space in their homes.

Robust student population and new house builds boost self storage interest in the Midwest

Self storage demand in the Midwest is on the rise, driven by a burgeoning population across the region’s urban and suburban areas. As more people flock to these communities, the need for additional storage space grows. Further intensifying this demand is the Midwest’s diverse climate, characterized by wide temperature fluctuations throughout the year. Whether it’s storing summer camping gear away from the winter chill or keeping delicate items safe from the summer heat, self storage offers a perfect solution. This blend of demographic trends and distinct seasonal needs makes self storage a crucial part of life in the Midwest.

Ann Arbor, MI, ranking seventh among the country’s high-demand areas for self storage, currently features about 5.4 square feet of space per capita and registers around 740 monthly Google searches per 10,000 residents related to this sector. The metro area has seen both population growth and an important increase in the number of households over the past 10 years. A major component of self storage demand in Ann Arbor is its large student population. The metro area ranks third among the 150 analyzed for Google searches related to self storage for students, only natural seeing as students represent about a fifth of the total number of residents.

Another metro area in Michigan that makes it to top 20 is Lansing-East Lansing, boasting a remarkable population growth of almost 16% as well as a healthy interest in self storage services, as shown by local Google searches. Currently, the Lansing metro area has an inventory of 6.4 square feet of storage space per capita.

Minneapolis-St. Paul-Bloomington, MN-WI, taking up the eighth position in our ranking, averages at 6.5 square feet of storage space per capita, below the national benchmark. The metro area has seen increases in both population and the number of households over the past 10 years. Also, Minneapolis showcases an active housing construction sector, with almost 18K building permits released in 2023 alone, a significant aspect as home buying and moving are strongly correlated with an increased demand for self storage services. The metro area also has almost 910K households with two cars or more, which adds up to self storage demand. Not only might a storage unit be needed for the extra car or cars in a household, but owning multiple cars also excludes the garage as a storage space for other items.

Population growth and a healthy interest for business storage services are among the factors pushing Lincoln, NE, to the sixteenth position in the ranking of the country’s most promising markets for self storage development. The residents of the metro area seem to be quite keen in maintaining their homes neat and tidy, boasting the third-highest volume of Googles searches related to decluttering among the metros analyzed.

With only five square feet of self storage space per capita and an average of 925 monthly Google searches per 10,000 residents for self storage services, Youngstown-Warren-Boardman, OH-PA, lands in fifteenth place.

California’s self storage gold rush starts in LA, with demand propelled by its hot housing market

Greater Los Angeles, with nearly 13 million residents, is the only California metro area in the top 20 showing major potential for self storage growth. This area offers just under five square feet of storage space per person, a figure pressured by multiple demand factors. It has the second-highest housing density among 150 analyzed metro areas and relatively small apartments, averaging 816 square feet. Despite years of outmigration and the issuance of 31,000 new housing permits in 2023 alone, the housing market remains highly competitive. Whether downsizing, renting or buying, there’s a lot of activity on the housing front, which supports extensive self storage use. Additionally, the remote work force in LA is a million strong, second only to New York City, further tightening living space for residents. Beyond these key drivers, LA’s enthusiasm for cars is notable — with 2.65 million households owning at least two cars, the demand for vehicle storage is robust.

Limited apartment space and dense housing conditions push three Pennsylvania metro areas into the top 20 most promising markets for development

Adding up to the East Coast and Midwest metro areas primed for self storage development, three Pennsylvanian urban hot spots make it to our top 20. Pittsburgh, PA, lands on 11, with 5.3 square feet of storage space per capita and almost 880 monthly Googe searches targeting self storage per 10,000 residents. Even if Pittsburgh’s population stayed about the same over the past decade, dense housing and small apartments (averaging around 790 square feet) are creating the right context for self storage to thrive. On top of that, Pittsburgh is also home to 125K students and over 200K remote workers, two categories of people who use self storage services, either short term or long term, to a higher degree than the average American. Harrisburg-Carlisle, PA, ranking thirteenth, has about the same amount of self storage space per capita as Pittsburgh and has more spacious apartments on average — however, it’s also more popular with newcomers, a known factor of increased self storage demand.

Philadelphia-Camdem-Wilmington, PA-NJ-DE, is second to last among the country’s top 20 metro areas primed for self storage development, currently featuring a modest five square feet of space per capita. Its relative affordability, particularly for a metro area its size, makes it an attractive destination for many. The number of households in the area increased by 12% over the past 10 years. This trend seems to hold up as house construction activity is flourishing in Philadelphia, with almost 13,500 housing units permitted in 2023, which will further encourage moving activity. Combined with dense housing conditions, relatively compact apartments and an appreciable number of both college students and remote workers, Philadelphia looks more than ready for the addition of new self storage space.

Bolstered by their thriving economies and lifestyle preferences, the largest urban hot spots in the Pacific Northwest are poised for more self storage space

The region’s dynamic population growth, fueled by factors such as job opportunities, lifestyle preferences and urbanization, is expected to keep contributing significantly to the need for storage solutions. The Pacific Northwest’s outdoor-centric lifestyle, with activities such as hiking, skiing and boating being popular year-round, creates a demand for storage of recreational equipment and gear — so it’s not surprising that the two major urban hot spots in the area are among the country’s most promising markets for further self storage development.

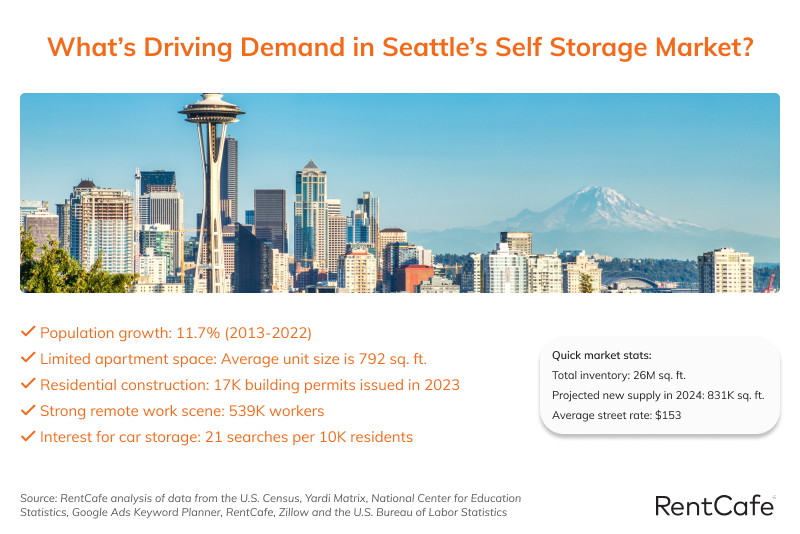

With new residents pouring in and an inventory of just under seven square feet of storage space per capita, Seattle-Tacoma-Belleview, WA, takes up the twelfth position in our ranking. The area registers almost 600 monthly searches for self storage services overall, and there are also high search volumes for specialized services such as car storage. The Seattle metro area also boasts the highest average household income among the top 20 metros, at $107K, signaling spending prowess that oftentimes translates into the need for extra storage, whether it’s purchasing boats or recreational vehicles, remodeling homes or collecting expensive items.

Portland-Vancouver-Hillsboro, OR-WA, features a local inventory that’s in line with the national benchmark. Local interest in the meantime is among the highest in the country, as shown by the 1,075 online searches per month targeting self storage related topics. The growing population, as well as the sustained home construction activity, are just some of the forces that are pushing on the local self storage inventory and are signaling development opportunities.

The flip side: the South reigns supreme as the country’s best supplied region for self storage

The southern U.S. has been in the midst of intense growth for a good while now, with a steady influx of new residents and new businesses reshaping its economic and demographic ecosystems. Many of the changes that occurred in our southern cities, from incoming migration and high levels of residential construction to an increasingly sophisticated and complex business environment, created just the right combination of factors to drive self storage demand up. However, unlike the cities that we discussed so far, self storage development in the southern metros kept a high enough pace so that it’s now mostly able to meet the local demand. In fact, the southern U.S. took up a significant share of the new self storage construction that occurred over the past decade nationwide, resulting in mostly generous self storage inventories across the region.

The area’s primary markets, including Dallas-Fort Worth-Arlington, TX, Houston-The Woodlands-Sugar Land, TX, and Atlanta-Sandy Springs-Alpharetta, GA, are all boasting per capita inventories of nine square feet and over.

The Dallas and Houston metro areas are both almost touching on 11 square feet of self storage space per capita, a much-needed supply level, we might say, when looking at the local demand drivers. Both metro areas experienced significant population growth of over 16% during the past decade, while the number of households also increased substantially over the same period, by 21% in the Dallas metro area and by 24% in the Houston metro area.

Even with the already robust self storage supply in both these Texan metros, new construction is still being planned — however, we might soon experience some tempering on this front in both markets. About 1.8M square feet of new self storage space is expected to be delivered in Dallas-Fort Worth-Arlington this year, but that amount represents only 2.4% of the existing inventory. Similarly, the Houston market is expected to increase its total inventory by just 1.7% in 2024.

Atlanta-Sandy Springs-Alpharetta, GA, is another primary market where self storage demand and supply converge to provide easily accessible and affordable services to local residents. Despite many signs of high demand, like the metro area’s recent 13% population growth, a large college student population and numerous households with multiple vehicles, the market is well positioned to meet demand. It currently offers nine square feet of storage space per capita.

Moving on to secondary markets where self storage demand meets the existing supply, we notice the same geographical trend, with most metro areas being from the South, with just one major exception. Sacramento-Roseville-Folsom, CA, which weathered a 9% population growth, stands out as a favorable place for self storage customers, with nine square feet of storage space per capita as well as demand surging from the almost 170,000 college students and the 225,000 remote workers. Other medium-sized metro areas, including San Antonio-New Braunfels, TX, and Las Vegas-Henderson-Paradise, NV, are also doing an excellent job in ensuring comfortable access to self storage services for their residents.

Among the tertiary markets, Lafayette, LA, is the country’s best positioned metro area to satisfy the local demand for self storage, with its almost 14 square feet of space per capita. Conversely, other tertiary markets with a well-developed self storage sector include Jackson, MS, and Corpus Christi, TX.

What the experts are saying

We've also discussed the current state of the US self-storage development market and the principal factors influencing it with Nicholas Malagisi, SIOR & National Director of Self Storage, Brian Dana from SVN Commercial Realty Advisors, and Doug Ressler, Business Intelligence Manager at Yardi Matrix.

Nicholas Malagisi, SIOR & National Director Self Storage, and Brian Dana, SVN Commercial Realty Advisors

About 18 months ago, just as the Federal Reserve began raising interest rates, I discussed with my SVN national self-storage team that transaction volume for stabilized self-storage assets would likely decrease significantly from the previous 3-4 years of record-high transaction volumes in our industry, which ranged between $16-18 billion. However, I predicted that transaction volumes for land/development deals would likely increase, given that not all planned projects would reach completion with the original developers due to the doubling of interest rates and/or the uncertainty of floating interest rates on construction loans. This prediction proved accurate, and last year we closed several deals on failed development projects with new developers who had either deep pockets or access to fixed-rate financing. Currently, we are marketing three additional 'approved' projects.

Yardi Matrix has recently confirmed that the national development pipeline for storage remains healthy with a 3-4% increase expected this year and into 2025. Land use, permissible zoning regulations, and requirements vary widely across the USA, presenting complex issues. In my first six years in the self-storage industry working for Public Storage in their corporate real estate department, I located self-storage sites and secured approvals for self-storage use where no such provisions existed in most municipal zoning codes. I often had to find parcels of land zoned 'Industrial' but with retail visibility to get local municipal approvals while meeting Public Storage's requirements for properties with visible/retail exposure.

Zoning requirements not only limit the use of self-storage in certain areas but may also restrict the ability to build a specific type of storage project. For example, suburban regulations might limit the size/scope of a development project through setback requirements or by imposing height and density restrictions. Urban planners utilize density limitations through the Floor Area Ratio (FAR), given that urban lot sizes are smaller compared to suburban acreage.

Land usage approvals can be 'allowed by right' or with a 'special exception,' such as the 'C-8' classification in Fairfax, VA, which imposes a 25% building-to-ground coverage ratio limitation, versus their I-4, I-5, and I-6 industrial zoning classifications that allow the use of self-storage by right but with varying degrees of density. Land usage can also be 'subjective' versus 'allowed by right,' where an architectural review board might be an additional hurdle, focusing not on the use of the land but on how the project/structure will appear. For instance, a board may require a self-storage project to be 'compatible' with the neighborhood aesthetics or mandate no overhead doors facing the street front. Additional limitations could include restricted operating hours or specific aesthetic preferences like prohibiting orange-colored doors on the project.

These types of zoning limitations are prevalent in more developed/urban areas or affluent municipalities that are particular about new developments in their neighborhoods. In essence, NIMBY (Not In My Back Yard) sentiments are still strong in certain areas where self-storage is considered a 'non-essential' use.

Self-storage demand has been steadily growing since its inception as a niche real estate product. The development community now recognizes that self-storage is not just a real estate product but an operating business driven by consumer needs. Demand is calculated primarily by two quantitative methods focused on the Primary Trade Area of a project—more on what constitutes a feasible site later.

It's crucial to note that introducing too much 'self-storage product' simultaneously as another competitor can disrupt a project's success. Once a self-storage project has 'stabilized,' it can perform financially as well as any other real estate sector. The most challenging time for any real estate project, particularly self-storage, is during the lease-up phase since there is no pre-leasing whatsoever. A self-storage project may take as long as 14-16 months to break even upon opening, and between 32-42 months to stabilize and allow the developer to refinance the construction loan. Self-storage has the lowest default rate of any type of real estate.

With self-storage demand returning to pre-COVID levels, developers today have access to more data than ever to make informed decisions about where to build and what kind of project to undertake to ensure success.

Doug Ressler, Business Intelligence Manager at Yardi Matrix

Amid economic headwinds, the self storage industry exhibits a stance of cautious optimism. Despite a noticeable reduction in new constructions compared to the 2019 peak, when 65 million square feet of storage space was added, the sector is gearing up to introduce an estimated 54 million square feet by the end of this year. This scale-back in development is a response to several pressing challenges currently facing the industry, including inflation and political unrest. These factors have contributed to a decline in occupancy rates by 2-3% and a 4-5% decrease in income from storage operations year-over-year.

However, the industry finds a silver lining as the economy is actually doing better than expected, giving the self storage sector solid ground to stand on for future growth. In fact, despite the downturn in some operational metrics, rental rates remain 8.7% higher than pre-pandemic levels.

Certain areas are even experiencing a surge in demand, particularly in academic and tertiary markets, opening up new avenues for capitalization and expansion.

___________

While the self storage sector has seen significant expansion in recent years, there are still vast regions across the country with untapped potential. From the urban centers of the Northeast to the sprawling suburbs of the Midwest, various areas are primed for investment in self storage infrastructure. As developers and investors look to capitalize on this burgeoning market, strategic expansion into underserved regions presents an opportunity to meet the evolving needs of customers nationwide and drive continued success in the self storage industry.

See how the 150 metro areas compare in terms of self storage provisions related to potential sources of demand in the table below.

Self Storage Stock and Key Demand Drivers in the US's 150 Largest Metro Areas

| Rank | Metro | Self Storage Per Capita (sq. ft.) | 2024 Completions as % of Existing Inventory | Online Self Storage Searches Per 10,000 Residents | Population Change 2013 - 2022 | Household Size | Household Formation Change 2013 - 2022 | Housing Density Per Square Mile | Residential Building Permits 2023 | Average Apartment Size | % of Apartments With Storage | Rental Competitivity Index | Homes For Sale Inventory Changes, 2018 - 2013 | Mobile Homes Inventory | Online Searches For Student Storage Per 10,000 Residents | No. of Students | Business Storage Searches Per 10,000 Residents | No. of Households With More Than One Car | No. of Vehicle Storage Units | Car Storage Searches Per 10,000 Residents | No. of Remote Workers | Decluttering Searches Per 10,000 Residents | Income Growth 2013 - 2022 | Household Income ($) | Unemployment Rate | Y-O-Y Employment Change | Self Storage Rent (10x10 Non-climate-controlled, $) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Springfield, MA | 3.7 | 16.20% | 755.4 | 10.80% | 2.4 | 18.20% | 485 | 624 | 739 | 0.00% | 13 | -57% | 4,138 | 1.1 | 66,096 | 3.31 | 150,076 | 76 | 17.13 | 38,340 | 9 | 31% | 68,400 | 3.6% | -1.04% | 117 |

| 2 | Honolulu, HI | 3.2 | 4.00% | 699.8 | 1.20% | 2.8 | 9.60% | 622 | 1,851 | 695 | 2.30% | 9 | -39% | 1,565 | 1.3 | 49,957 | 1.42 | 187,835 | 201 | 18.22 | 45,632 | 4.1 | 32% | 96,580 | 2.6% | 0.09% | 277 |

| 3 | Boulder, CO | 6.3 | 0.00% | 998.1 | 5.60% | 2.3 | 11.60% | 199 | 1,646 | 863 | 46.70% | 9 | -20% | 3,261 | 2.68 | 49,603 | 3.83 | 86,749 | 310 | 13.98 | 57,679 | 9.2 | 34% | 96,079 | 3.2% | 0.13% | 151 |

| 4 | Providence-Warwick, RI-MA | 4.8 | 9.20% | 830.5 | 4.30% | 2.4 | 9.80% | 461 | 1,909 | 772 | 1.30% | 15 | -66% | 6,668 | 1.36 | 91,902 | 1.79 | 370,836 | 474 | 19.88 | 107,951 | 3.8 | 49% | 81,784 | 3.7% | 1.07% | 130 |

| 5 | Greeley, CO | 7.6 | 7.20% | 1,004.70 | 29.80% | 2.8 | 34.00% | 32 | 3,719 | 865 | 29.10% | 9 | -20% | 8,599 | 1.32 | 16,558 | 4.16 | 92,047 | 1,022 | 13.61 | 26,262 | 8.9 | 56% | 91,565 | 3.6% | 0.30% | 114 |

| 6 | Rochester, NY | 5.2 | 0.50% | 916 | -0.20% | 2.3 | 7.20% | 169 | 1,560 | 859 | 3.90% | 9 | -58% | 16,177 | 2.03 | 64,466 | 2.44 | 245,996 | 393 | 21.42 | 72,935 | 5.6 | 34% | 69,580 | 3.9% | 1.20% | 110 |

| 7 | Ann Arbor, MI | 5.4 | 0.00% | 738.9 | 3.40% | 2.3 | 9.60% | 226 | 1,303 | 866 | 11.80% | 7 | -51% | 7,338 | 3.01 | 77,068 | 3.54 | 82,650 | 422 | 16.46 | 41,166 | 9 | 34% | 79,665 | 3.2% | 5.38% | 105 |

| 8 | Minneapolis-St. Paul-Bloomington, MN-WI | 6.5 | 2.50% | 805.9 | 6.80% | 2.4 | 11.40% | 220 | 17,943 | 850 | 2.20% | 9 | -45% | 21,853 | 0.44 | 243,427 | 0.56 | 907,876 | 2,215 | 18.18 | 412,170 | 1.9 | 36% | 91,341 | 2.7% | 0.65% | 99 |

| 9 | Phoenix-Mesa-Chandler, AZ | 8.4 | 3.80% | 1,192.60 | 14.00% | 2.6 | 21.70% | 142 | 45,637 | 847 | 63.10% | 8 | -33% | 113,017 | 0.4 | 488,465 | 1.07 | 1,159,921 | 6,040 | 20.96 | 531,371 | 1.4 | 60% | 82,884 | 3.6% | 2.30% | 113 |

| 10 | Los Angeles-Long Beach-Anaheim, CA | 4.9 | 2.50% | 417.3 | -2.00% | 2.8 | 5.90% | 987 | 30,691 | 816 | 38.20% | 12 | -43% | 87,293 | 0.16 | 932,469 | 0.95 | 2,648,931 | 7,373 | 16.16 | 1,092,654 | 1.4 | 49% | 87,743 | 5.0% | -0.79% | 201 |

| 11 | Pittsburgh, PA | 5.3 | 0.40% | 878.3 | -0.50% | 2.2 | 3.40% | 201 | 5,423 | 791 | 5.00% | 6 | -50% | 36,955 | 0.68 | 125,084 | 0.74 | 543,552 | 1,258 | 7.87 | 201,109 | 2.2 | 38% | 70,607 | 3.2% | 1.25% | 114 |

| 12 | Seattle-Tacoma-Bellevue, WA | 6.9 | 3.10% | 599.5 | 11.70% | 2.5 | 15.70% | 291 | 17,254 | 792 | 39.90% | 9 | -42% | 46,226 | 0.3 | 168,017 | 0.52 | 928,449 | 3,660 | 20.98 | 539,160 | 1.8 | 58% | 106,909 | 4.2% | 0.52% | 153 |

| 13 | Harrisburg-Carlisle, PA | 5.4 | 0.00% | 612.2 | 8.20% | 2.4 | 10.10% | 159 | 1,883 | 928 | 6.90% | 13 | -62% | 9,174 | 1.14 | 31,703 | 2.19 | 145,677 | 230 | 7.39 | 50,604 | 5.2 | 31% | 73,739 | 2.8% | 2.06% | 103 |

| 14 | Denver-Aurora-Lakewood, CO | 7.3 | 1.40% | 948.2 | 10.70% | 2.4 | 18.20% | 155 | 20,623 | 850 | 36.00% | 9 | -23% | 18,490 | 0.34 | 149,433 | 0.55 | 758,741 | 2,407 | 12.17 | 397,525 | 1.3 | 58% | 98,975 | 3.5% | -0.69% | 122 |

| 15 | Youngstown-Warren-Boardman, OH-PA | 5 | 0.00% | 924.7 | -3.60% | 2.3 | 0.30% | 246 | 299 | 805 | 3.30% | 11 | -57% | 8,362 | 0.64 | 14,263 | 2.87 | 128,916 | 182 | 14.81 | 18,675 | 8.1 | 30% | 54,506 | 4.3% | 0.02% | 84 |

| 16 | Lincoln, NE | 6.3 | 0.00% | 505.2 | 7.70% | 2.4 | 12.40% | 104 | 2,140 | 923 | 18.30% | 12 | -48% | 2,278 | 2.72 | 39,437 | 4.94 | 82,498 | 456 | 12.1 | 20,893 | 12.1 | 29% | 67,235 | 2.2% | 0.62% | 100 |

| 17 | Lansing-East Lansing, MI | 6.4 | 8.40% | 961.9 | 15.70% | 2.3 | 21.80% | 140 | 952 | 876 | 9.10% | 7 | -55% | 11,753 | 1.85 | 65,318 | 2.65 | 127,691 | 364 | 9.67 | 40,158 | 7.2 | 31% | 64,478 | 3.7% | 5.49% | 91 |

| 18 | Portland-Vancouver-Hillsboro, OR-WA | 7.4 | 2.10% | 1,075.60 | 8.40% | 2.4 | 14.70% | 159 | 11,294 | 826 | 47.10% | 8 | -40% | 37,736 | 0.61 | 87,848 | 0.72 | 592,445 | 2,187 | 13.28 | 303,293 | 2.3 | 51% | 89,312 | 4.0% | -0.77% | 135 |

| 19 | Philadelphia-Camden-Wilmington, PA-NJ-DE-MD | 5 | 4.60% | 464.4 | 3.40% | 2.5 | 12.00% | 572 | 13,476 | 838 | 6.70% | 9 | -54% | 29,312 | 0.26 | 314,549 | 0.39 | 1,289,709 | 2,593 | 9.34 | 582,459 | 1.4 | 39% | 84,123 | 3.6% | 1.82% | 122 |

| 20 | Worcester, MA-CT | 5.4 | 15.00% | 567.1 | 5.80% | 2.5 | 11.50% | 268 | 1,388 | 862 | 2.50% | 13 | -57% | 4,609 | 1.52 | 46,902 | 2.19 | 220,690 | 404 | 16.38 | 76,136 | 5 | 36% | 83,891 | 3.3% | -0.12% | 122 |

| 21 | Boston-Cambridge-Newton, MA-NH | 4.7 | 3.00% | 311.9 | 4.60% | 2.4 | 10.50% | 592 | 10,580 | 824 | 6.70% | 12 | -46% | 21,950 | 0.3 | 350,532 | 0.27 | 991,669 | 1,570 | 6.02 | 547,117 | 1 | 43% | 104,299 | 2.9% | 0.74% | 145 |

| 22 | Salinas, CA | 6 | 0.00% | 444.3 | 0.90% | 3.1 | 5.50% | 44 | 595 | 837 | 14.30% | 13 | -52% | 5,783 | 2.28 | 23,554 | 4.57 | 91,734 | 237 | 11.42 | 22,115 | 11 | 63% | 92,840 | 7.2% | -0.79% | 212 |

| 23 | Salt Lake City, UT | 8.4 | 1.30% | 1,120.30 | 11.00% | 2.8 | 22.20% | 61 | 9,199 | 863 | 33.10% | 9 | -23% | 9,817 | 0.56 | 230,407 | 0.75 | 300,507 | 975 | 11.68 | 128,873 | 2.3 | 49% | 91,891 | 2.9% | 1.70% | 116 |

| 24 | Madison, WI | 6.7 | 5.00% | 790.1 | 9.50% | 2.2 | 17.50% | 95 | 5,255 | 850 | 4.70% | 17 | -57% | 3,185 | 1.36 | 67,287 | 1.64 | 172,941 | 459 | 10.36 | 72,911 | 4.1 | 40% | 83,214 | 2.3% | 2.76% | 94 |

| 25 | San Jose-Sunnyvale-Santa Clara, CA | 5.4 | 0.60% | 368.6 | 1.00% | 2.8 | 6.40% | 268 | 6,288 | 839 | 48.40% | 11 | -36% | 19,277 | 0.43 | 128,158 | 0.41 | 424,777 | 692 | 12.93 | 243,584 | 1.4 | 63% | 148,900 | 4.1% | -2.14% | 177 |

| 26 | Toledo, OH | 6.4 | 0.30% | 987.1 | 5.30% | 2.3 | 14.20% | 224 | 1,352 | 811 | 9.60% | 6 | -57% | 13,214 | 0.45 | 48,545 | 2 | 158,783 | 335 | 10.64 | 23,912 | 4.8 | 43% | 61,012 | 4.2% | 0.49% | 93 |

| 27 | San Francisco-Oakland-Berkeley, CA | 5.1 | 0.70% | 303.5 | 1.40% | 2.6 | 5.10% | 760 | 7,478 | 778 | 35.40% | 8 | -22% | 17,579 | 0.23 | 258,403 | 0.25 | 932,340 | 1,885 | 4.43 | 636,052 | 1.1 | 61% | 128,151 | 4.2% | -1.97% | 207 |

| 28 | Allentown-Bethlehem-Easton, PA-NJ | 4.6 | 3.90% | 377.6 | 5.30% | 2.5 | 7.90% | 249 | 1,772 | 854 | 5.90% | 14 | -63% | 8,083 | 0.92 | 40,200 | 1.64 | 197,506 | 601 | 8.25 | 53,130 | 3.8 | 34% | 76,041 | 3.7% | 1.29% | 129 |

| 29 | York-Hanover, PA | 5.4 | 20.20% | 715.5 | 5.00% | 2.5 | 11.60% | 210 | 1,143 | 876 | 11.60% | 13 | -60% | 6,977 | 1.04 | 4,925 | 3.48 | 123,989 | 364 | 8.52 | 29,767 | 8 | 40% | 80,130 | 3.0% | 1.91% | 107 |

| 30 | New York-Newark-Jersey City, NY-NJ-PA | 3.7 | 4.10% | 294.1 | -1.70% | 2.6 | 5.60% | 1,315 | 39,941 | 788 | 2.30% | 6 | -49% | 38,573 | 0.19 | 932,934 | 0.4 | 2,690,037 | 4,866 | 8.69 | 1,562,742 | 1.2 | 39% | 91,562 | 4.5% | -0.01% | 182 |

| 31 | Cincinnati, OH-KY-IN | 6.3 | 3.40% | 689.6 | 6.30% | 2.4 | 11.50% | 222 | 6,246 | 881 | 12.40% | 11 | -51% | 29,343 | 0.52 | 121,927 | 1.24 | 563,703 | 2,566 | 9.28 | 171,445 | 2.1 | 41% | 75,062 | 3.4% | 0.46% | 92 |

| 32 | Canton-Massillon, OH | 6.6 | 0.00% | 1,034.30 | -1.10% | 2.4 | 3.90% | 187 | 509 | 834 | 34.60% | 6 | -54% | 4,619 | 1.06 | 19,577 | 4.66 | 100,813 | 166 | 12.71 | 20,408 | 10.6 | 43% | 64,546 | 3.8% | 0.47% | 83 |

| 33 | Washington-Arlington-Alexandria, DC-VA-MD-WV | 5.7 | 2.20% | 131.8 | 7.10% | 2.6 | 13.60% | 423 | 23,034 | 863 | 12.10% | 9 | -54% | 14,245 | 0.24 | 406,009 | 0.28 | 1,326,847 | 1,907 | 3.69 | 866,858 | 0.9 | 30% | 117,432 | 2.7% | 1.69% | 143 |

| 34 | Chicago-Naperville-Elgin, IL-IN-WI | 5.5 | 1.30% | 353 | -1.00% | 2.5 | 8.00% | 573 | 14,821 | 787 | 9.80% | 12 | -51% | 38,855 | 0.2 | 482,305 | 0.81 | 1,897,032 | 5,249 | 12.79 | 826,975 | 1.2 | 37% | 82,914 | 4.6% | -0.94% | 104 |

| 35 | Detroit-Warren-Dearborn, MI | 5.4 | 4.10% | 715.8 | 1.20% | 2.4 | 6.30% | 492 | 6,197 | 877 | 7.20% | 8 | -37% | 55,954 | 0.32 | 130,324 | 0.51 | 970,887 | 2,993 | 15.5 | 335,226 | 1.3 | 37% | 71,265 | 3.8% | 2.00% | 110 |

| 36 | Grand Rapids-Kentwood, MI | 6.6 | 0.60% | 563.7 | 7.60% | 2.6 | 12.10% | 136 | 3,716 | 886 | 17.20% | 9 | -57% | 25,073 | 0.71 | 51,718 | 1.04 | 267,451 | 776 | 5.93 | 69,180 | 2.5 | 48% | 77,771 | 3.1% | 4.71% | 100 |

| 37 | San Diego-Chula Vista-Carlsbad, CA | 6.3 | 1.60% | 378.8 | 2.00% | 2.7 | 7.20% | 296 | 11,468 | 842 | 47.80% | 13 | -54% | 39,625 | 0.51 | 300,212 | 0.45 | 753,433 | 2,173 | 15.4 | 308,923 | 1.4 | 61% | 98,928 | 4.4% | -1.37% | 176 |

| 38 | Columbus, OH | 6.7 | 4.40% | 668.2 | 9.90% | 2.4 | 15.20% | 193 | 11,439 | 902 | 4.20% | 7 | -43% | 21,867 | 0.51 | 121,202 | 0.81 | 509,286 | 1,584 | 8.64 | 203,852 | 1.7 | 40% | 75,777 | 3.2% | 0.47% | 91 |

| 39 | Spartanburg, SC | 7.2 | 3.30% | 832.4 | 8.40% | 2.5 | 11.00% | 109 | 2,867 | 924 | 37.80% | 9 | -51% | 19,845 | 1.99 | 15,683 | 3.58 | 85,953 | 491 | 7.55 | 14,845 | 8.9 | 41% | 57,755 | 3.1% | 3.88% | 84 |

| 40 | Trenton-Princeton, NJ | 4.3 | 15.50% | 302.3 | 2.80% | 2.5 | 10.20% | 673 | 978 | 863 | 1.60% | 9 | -67% | 485 | 1.7 | 34,917 | 2.69 | 76,931 | 178 | 9.92 | 34,925 | 7.4 | 35% | 95,668 | 4.0% | -0.76% | 136 |

| 41 | Lakeland-Winter Haven, FL | 8.5 | 10.30% | 983.3 | 26.40% | 2.6 | 36.10% | 190 | 12,513 | 962 | 29.00% | 10 | 1% | 63,605 | 0.88 | 25,080 | 2.3 | 161,125 | 915 | 8.5 | 42,260 | 4.6 | 46% | 62,051 | 3.9% | 1.13% | 101 |

| 42 | Provo-Orem, UT | 9.5 | 1.10% | 1,014.10 | 27.10% | 3.4 | 39.50% | 40 | 6,175 | 954 | 33.50% | 9 | 0% | 2,134 | 1.71 | 79,848 | 2.62 | 164,297 | 870 | 8.09 | 68,706 | 5.7 | 59% | 95,687 | 2.8% | 0.91% | 93 |

| 43 | McAllen-Edinburg-Mission, TX | 6.4 | 8.00% | 421.4 | 8.90% | 3.3 | 21.30% | 196 | 6,625 | 899 | 30.20% | 5 | 2% | 41,985 | 0.35 | 60,783 | 2.1 | 170,063 | 592 | 5.72 | 31,963 | 5.5 | 40% | 49,142 | 5.8% | 2.35% | 90 |

| 44 | Winston-Salem, NC | 6.9 | 2.90% | 770.4 | 5.80% | 2.4 | 8.80% | 154 | 5,028 | 907 | 29.40% | 8 | -46% | 29,759 | 1.04 | 28,627 | 2.4 | 181,392 | 575 | 9.81 | 37,465 | 5.8 | 45% | 61,556 | 3.4% | 1.62% | 95 |

| 45 | Tampa-St. Petersburg-Clearwater, FL | 8.3 | 5.60% | 851.1 | 14.60% | 2.4 | 16.60% | 601 | 25,395 | 924 | 34.50% | 10 | -30% | 151,850 | 0.33 | 137,113 | 0.54 | 707,612 | 3,635 | 18.01 | 333,620 | 1 | 51% | 69,290 | 3.2% | 1.86% | 113 |

| 46 | Tucson, AZ | 8.3 | 5.00% | 1,070.20 | 6.10% | 2.4 | 11.40% | 52 | 5,255 | 770 | 58.00% | 7 | -43% | 41,615 | 1.55 | 69,432 | 2.16 | 240,927 | 1,767 | 17.76 | 69,188 | 4.7 | 46% | 64,014 | 3.9% | 1.19% | 112 |

| 47 | Anchorage, AK | 7.3 | 0.00% | 801.6 | 1.10% | 2.6 | 12.00% | 7 | 373 | 886 | 6.00% | 11 | -66% | 5,111 | 1.09 | 11,366 | 4.64 | 95,727 | 333 | 16.67 | 23,812 | 14.2 | 25% | 95,791 | 4.1% | -0.88% | 161 |

| 48 | South Bend-Mishawaka, IN-MI | 6 | 5.30% | 1,088.00 | 1.60% | 2.5 | 3.40% | 152 | 434 | 905 | 14.40% | 6 | -48% | 4,067 | 1.4 | 22,740 | 2.3 | 73,238 | 41 | 11.7 | 13,295 | 5.2 | 49% | 60,772 | 4.1% | -0.75% | 98 |

| 49 | Gainesville, FL | 8.4 | 7.20% | 861.7 | 28.40% | 2.3 | 37.20% | 67 | 2,267 | 1,005 | 18.80% | 7 | -29% | 21,276 | 1.55 | 73,715 | 4.15 | 77,957 | 275 | 12.44 | 21,457 | 8.6 | 54% | 59,516 | 3.3% | 1.86% | 106 |

| 50 | Cleveland-Elyria, OH | 5.2 | 1.70% | 480.3 | -0.10% | 2.3 | 5.60% | 360 | 3,276 | 814 | 1.30% | 6 | -57% | 9,647 | 0.51 | 74,005 | 0.57 | 464,029 | 1,204 | 7.6 | 155,990 | 1.3 | 32% | 65,198 | 3.8% | 0.52% | 101 |

| 51 | Buffalo-Cheektowaga, NY | 4.3 | 4.60% | 315.8 | 2.40% | 2.2 | 7.60% | 346 | 1,292 | 805 | 9.10% | 9 | -48% | 11,046 | 0.52 | 75,663 | 0.59 | 248,508 | 806 | 7.28 | 72,130 | 1.4 | 36% | 68,698 | 4.1% | 1.30% | 108 |

| 52 | Akron, OH | 6.2 | 1.90% | 756.4 | -1.10% | 2.3 | 4.80% | 354 | 985 | 873 | 1.90% | 6 | -58% | 6,940 | 0.82 | 42,180 | 2.25 | 167,942 | 440 | 11.85 | 53,503 | 5.1 | 33% | 66,652 | 3.7% | 2.11% | 90 |

| 53 | El Paso, TX | 6.1 | 2.80% | 310.3 | 4.70% | 2.9 | 16.10% | 58 | 2,265 | 829 | 33.40% | 12 | -44% | 17,640 | 0.34 | 53,353 | 1.28 | 189,712 | 718 | 4.19 | 33,656 | 3.1 | 34% | 53,359 | 4.4% | 1.35% | 95 |

| 54 | Indianapolis-Carmel-Anderson, IN | 8.4 | 1.90% | 790.9 | 9.70% | 2.5 | 15.30% | 225 | 12,588 | 891 | 36.70% | 6 | -35% | 21,050 | 0.53 | 136,294 | 0.77 | 515,932 | 2,100 | 8.61 | 164,044 | 1.6 | 48% | 75,824 | 3.1% | -0.38% | 85 |

| 55 | Riverside-San Bernardino-Ontario, CA | 7.8 | 1.40% | 415.7 | 6.50% | 3.2 | 11.30% | 59 | 19,710 | 854 | 54.50% | 11 | -45% | 117,316 | 0.41 | 201,867 | 0.49 | 1,016,031 | 6,836 | 13.69 | 237,670 | 1.5 | 56% | 82,803 | 5.3% | -1.15% | 126 |

| 56 | Durham-Chapel Hill, NC | 8.3 | 4.70% | 475.8 | 24.30% | 2.3 | 30.50% | 167 | 7,243 | 931 | 44.60% | 8 | -33% | 15,326 | 1.27 | 62,888 | 1.74 | 165,716 | 571 | 5.71 | 73,631 | 4 | 48% | 79,154 | 3.0% | 3.39% | 100 |

| 57 | Greenville-Anderson, SC | 8.9 | 0.60% | 969.8 | 12.70% | 2.4 | 20.80% | 156 | 7,728 | 973 | 25.70% | 9 | -45% | 50,528 | 1.22 | 61,474 | 1.73 | 249,117 | 1,074 | 8.36 | 48,838 | 4 | 46% | 65,681 | 2.9% | 3.02% | 84 |

| 58 | Ocala, FL | 8.7 | 2.90% | 897.5 | 17.50% | 2.4 | 22.90% | 118 | 5,197 | 993 | 25.70% | 7 | -18% | 37,403 | 0.88 | 13,957 | 3.39 | 89,913 | 729 | 9 | 18,504 | 7.5 | 40% | 54,190 | 3.9% | 1.34% | 95 |

| 59 | Wichita, KS | 7.6 | 0.20% | 626.4 | 1.90% | 2.5 | 4.20% | 67 | 2,676 | 789 | 8.40% | 8 | -55% | 11,093 | 1.22 | 34,304 | 2.81 | 163,282 | 804 | 7.45 | 24,940 | 6.2 | 35% | 67,012 | 3.1% | -0.26% | 85 |

| 60 | Miami-Fort Lauderdale-Pompano Beach, FL | 7 | 2.80% | 312.1 | 5.30% | 2.6 | 15.30% | 530 | 21,329 | 930 | 13.70% | 14 | -37% | 54,206 | 0.26 | 291,628 | 0.42 | 1,212,859 | 4,492 | 8.81 | 451,884 | 0.9 | 51% | 70,769 | 2.5% | 1.81% | 149 |

| 61 | Olympia-Lacey-Tumwater, WA | 9.2 | 0.00% | 635.1 | 13.90% | 2.5 | 18.80% | 173 | 1,512 | 841 | 57.70% | 9 | -45% | 9,315 | 1.24 | 7,502 | 4.21 | 76,331 | 375 | 15.1 | 28,942 | 11.9 | 49% | 88,853 | 4.7% | 0.18% | 150 |

| 62 | Des Moines-West Des Moines, IA | 8.1 | 1.20% | 348.3 | 21.60% | 2.4 | 27.10% | 87 | 5,017 | 853 | 13.60% | 10 | -52% | 6,399 | 0.5 | 32,186 | 0.92 | 187,811 | 673 | 3.77 | 59,480 | 2.2 | 31% | 80,061 | 2.9% | -1.11% | 83 |

| 63 | Deltona-Daytona Beach-Ormond Beach, FL | 9.3 | 8.60% | 1,478.60 | 17.50% | 2.3 | 25.70% | 216 | 7,097 | 932 | 17.10% | 7 | -25% | 28,280 | 1.5 | 40,294 | 2.5 | 163,965 | 1,081 | 11.59 | 49,453 | 5.5 | 59% | 65,889 | 3.5% | 1.70% | 127 |

| 64 | Santa Maria-Santa Barbara, CA | 8.1 | 1.80% | 468 | 1.90% | 2.8 | 7.20% | 59 | 449 | 766 | 19.10% | 13 | -56% | 7,516 | 3.39 | 53,534 | 5.51 | 94,958 | 258 | 12.71 | 27,638 | 10.8 | 46% | 90,894 | 4.4% | -1.36% | 192 |

| 65 | Dayton-Kettering, OH | 7.1 | 5.20% | 1,113.50 | 1.30% | 2.3 | 7.50% | 291 | 1,760 | 865 | 14.30% | 7 | -50% | 3,025 | 0.91 | 57,203 | 1.9 | 197,069 | 606 | 9.83 | 48,218 | 4.8 | 42% | 66,770 | 3.6% | 0.67% | 96 |

| 66 | Milwaukee-Waukesha, WI | 7.2 | 1.70% | 797.2 | -0.60% | 2.4 | 5.10% | 479 | 2,517 | 880 | 4.70% | 13 | -36% | 3,697 | 0.62 | 74,492 | 1.28 | 345,382 | 1,307 | 18.95 | 115,444 | 2.8 | 36% | 70,898 | 3.4% | 1.62% | 91 |

| 67 | Kennewick-Richland, WA | 9.4 | 1.10% | 842 | 14.90% | 2.8 | 17.00% | 39 | 2,059 | 857 | 39.90% | 8 | -39% | 10,057 | 0.75 | 6,216 | 4.23 | 76,948 | 301 | 12.19 | 16,485 | 11.4 | 42% | 82,961 | 5.1% | -0.30% | 116 |

| 68 | St. Louis, MO-IL | 6.7 | 3.40% | 745.5 | 0.00% | 2.4 | 5.70% | 162 | 7,300 | 872 | 19.50% | 6 | -57% | 37,723 | 0.45 | 143,337 | 0.64 | 696,706 | 2,262 | 13.99 | 221,510 | 1.9 | 37% | 74,531 | 3.5% | 0.59% | 91 |

| 69 | Portland-South Portland, ME | 9.1 | 5.50% | 1,059.10 | 8.00% | 2.3 | 13.60% | 138 | 2,972 | 804 | 3.50% | 17 | -60% | 12,839 | 1.23 | 29,897 | 2.08 | 146,412 | 395 | 19.53 | 57,540 | 5.4 | 54% | 84,312 | 2.7% | 3.16% | 127 |

| 70 | Baltimore-Columbia-Towson, MD | 6.3 | 3.60% | 222.9 | 2.30% | 2.5 | 8.50% | 462 | 7,236 | 864 | 22.40% | 8 | -58% | 11,711 | 0.43 | 157,340 | 0.41 | 622,241 | 1,277 | 5.66 | 262,005 | 1.2 | 32% | 90,505 | 2.3% | 1.50% | 126 |

| 71 | Richmond, VA | 8.8 | 3.10% | 825.2 | 7.40% | 2.4 | 15.20% | 131 | 9,976 | 880 | 18.50% | 10 | -56% | 11,709 | 1.1 | 60,369 | 1.2 | 337,502 | 667 | 7.15 | 127,864 | 3.1 | 42% | 81,388 | 3.0% | 3.27% | 105 |

| 72 | Port St Lucie, FL | 8.8 | 5.00% | 470.3 | 18.90% | 2.6 | 21.20% | 218 | 6,137 | 983 | 13.70% | 7 | -25% | 21,038 | 0.74 | 15,731 | 3.19 | 115,645 | 382 | 14.23 | 31,876 | 6.3 | 51% | 68,460 | 3.6% | 2.15% | 105 |

| 73 | Stockton, CA | 7.9 | 7.50% | 317.5 | 12.60% | 3.2 | 11.80% | 186 | 2,170 | 817 | 30.00% | 9 | -38% | 8,242 | 1.43 | 23,338 | 2.29 | 164,774 | 724 | 6.86 | 37,857 | 5 | 67% | 86,056 | 6.8% | -1.40% | 121 |

| 74 | Orlando-Kissimmee-Sanford, FL | 8.6 | 3.60% | 431.6 | 21.90% | 2.6 | 35.10% | 328 | 25,774 | 960 | 27.10% | 11 | -27% | 66,742 | 0.22 | 175,014 | 0.43 | 623,266 | 2,953 | 6.38 | 263,698 | 0.7 | 53% | 71,857 | 3.1% | 2.19% | 105 |

| 75 | Kansas City, MO-KS | 8 | 5.90% | 830.7 | 7.70% | 2.4 | 12.30% | 132 | 7,473 | 881 | 27.30% | 8 | -58% | 13,857 | 0.41 | 75,360 | 0.75 | 544,939 | 2,189 | 8.55 | 198,687 | 1.8 | 34% | 75,280 | 3.1% | 0.13% | 94 |

| 76 | Fort Collins, CO | 9.8 | 5.50% | 1,369.90 | 16.10% | 2.3 | 24.60% | 63 | 2,681 | 915 | 34.70% | 9 | -31% | 6,336 | 1.97 | 33,787 | 4.12 | 105,191 | 657 | 10.93 | 37,152 | 9.1 | 50% | 88,403 | 3.1% | 2.58% | 111 |

| 77 | Merced, CA | 7 | 2.50% | 271.6 | 10.20% | 3.3 | 13.10% | 47 | 404 | 907 | 28.90% | 9 | -32% | 4,399 | 0.26 | 19,317 | 3.36 | 61,876 | 353 | 6.72 | 7,797 | 9.3 | 63% | 66,164 | 9.8% | -1.34% | 121 |

| 78 | Jacksonville, FL | 10.1 | 5.60% | 1,202.10 | 20.20% | 2.5 | 30.20% | 229 | 20,253 | 952 | 31.30% | 7 | -27% | 44,206 | 0.66 | 47,143 | 1.03 | 398,476 | 1,986 | 16.28 | 155,280 | 2.3 | 51% | 77,583 | 3.1% | 2.10% | 115 |

| 79 | Charleston-North Charleston, SC | 10.4 | 4.10% | 1,259.90 | 16.60% | 2.4 | 26.10% | 146 | 8,496 | 958 | 23.10% | 8 | -52% | 32,695 | 1.27 | 34,118 | 2.36 | 210,440 | 1,020 | 16.18 | 61,743 | 5 | 52% | 78,927 | 2.6% | 6.50% | 102 |

| 80 | Brownsville-Harlingen, TX | 7.1 | 4.80% | 387 | 1.90% | 3.1 | 16.40% | 179 | 1,958 | 856 | 25.00% | 5 | -46% | 14,487 | 1.08 | 7,648 | 3.9 | 82,923 | 493 | 8.24 | 14,579 | 7.6 | 47% | 50,649 | 5.2% | 2.31% | 82 |

| 81 | College Station-Bryan, TX | 9.7 | 0.00% | 700.8 | 16.80% | 2.4 | 27.80% | 57 | 1,443 | 952 | 29.30% | 9 | -30% | 10,451 | 2.68 | 74,014 | 5.09 | 65,907 | 361 | 12.87 | 16,576 | 11 | 53% | 60,804 | 3.1% | 3.02% | 89 |

| 82 | Albany-Schenectady-Troy, NY | 6.6 | 3.10% | 500.4 | 3.00% | 2.3 | 9.20% | 150 | 1,952 | 896 | 5.30% | 11 | -43% | 12,973 | 0.67 | 81,169 | 0.89 | 199,364 | 520 | 7.74 | 67,746 | 2.5 | 36% | 80,970 | 3.4% | 1.01% | 113 |

| 83 | Colorado Springs, CO | 11.3 | 3.00% | 1,702.00 | 12.80% | 2.4 | 22.20% | 119 | 5,291 | 847 | 36.90% | 7 | -19% | 11,954 | 1.8 | 56,067 | 2.7 | 208,158 | 1,448 | 21.1 | 70,067 | 5.7 | 42% | 81,912 | 3.6% | 1.18% | 104 |

| 84 | Salem, OR | 9.8 | 0.00% | 963.6 | 9.00% | 2.6 | 13.50% | 87 | 1,987 | 873 | 29.50% | 8 | -48% | 10,755 | 1.28 | 14,385 | 3.35 | 103,255 | 577 | 9.57 | 25,718 | 8.1 | 53% | 72,150 | 4.1% | 0.30% | 129 |

| 85 | Palm Bay-Melbourne-Titusville, FL | 10.4 | 12.60% | 1,466.60 | 14.50% | 2.4 | 17.10% | 295 | 6,534 | 943 | 21.60% | 11 | -30% | 20,266 | 1.74 | 22,659 | 2.9 | 153,058 | 984 | 35.31 | 46,972 | 5.8 | 62% | 75,320 | 3.2% | 1.74% | 120 |

| 86 | Myrtle Beach-Conway-North Myrtle Beach, SC-NC | 12.4 | 2.40% | 1,424.20 | 32.40% | 2.3 | 42.50% | 278 | 13,072 | 989 | 32.80% | 8 | -41% | 41,464 | 1.69 | 20,639 | 4.31 | 146,810 | 429 | 13.48 | 29,941 | 9.4 | 49% | 64,741 | 3.5% | 4.44% | 96 |

| 87 | Raleigh-Cary, NC | 8.7 | 1.30% | 281.1 | 22.20% | 2.6 | 24.40% | 291 | 20,619 | 968 | 52.90% | 8 | -37% | 32,721 | 0.31 | 71,858 | 0.39 | 365,527 | 1,530 | 4.17 | 203,600 | 1.2 | 50% | 92,739 | 3.1% | 3.83% | 93 |

| 88 | Atlanta-Sandy Springs-Alpharetta, GA | 9 | 4.10% | 669.9 | 12.60% | 2.7 | 18.30% | 283 | 38,589 | 997 | 38.00% | 8 | -33% | 62,038 | 0.18 | 256,233 | 0.85 | 1,434,808 | 5,403 | 10.31 | 659,991 | 1.1 | 52% | 84,876 | 3.1% | 1.66% | 99 |

| 89 | Vallejo, CA | 9 | 1.20% | 606.6 | 5.60% | 2.8 | 11.70% | 200 | 1,416 | 837 | 57.10% | 9 | -39% | 4,494 | 2.26 | 10,419 | 3.65 | 109,433 | 648 | 12.15 | 26,569 | 9 | 46% | 92,959 | 5.1% | -0.72% | 164 |

| 90 | Charlotte-Concord-Gastonia, NC-SC | 8.9 | 3.50% | 528.5 | 18.00% | 2.5 | 26.30% | 208 | 29,361 | 943 | 35.60% | 8 | -29% | 68,841 | 0.3 | 93,244 | 0.4 | 680,364 | 2,704 | 5.63 | 313,624 | 1 | 51% | 77,154 | 3.3% | 2.62% | 95 |

| 91 | Fort Wayne, IN | 7.3 | 4.50% | 804.9 | 0.50% | 2.5 | 1.80% | 133 | 2,493 | 882 | 22.50% | 7 | -49% | 4,952 | 0.33 | 16,537 | 3.12 | 104,553 | 204 | 8.05 | 20,148 | 7.9 | 43% | 65,678 | 3.2% | -0.77% | 91 |

| 92 | Oxnard-Thousand Oaks-Ventura, CA | 7.8 | 1.00% | 509.6 | -0.80% | 2.9 | 4.80% | 161 | 1,089 | 865 | 46.70% | 11 | -52% | 11,137 | 1.21 | 39,896 | 1.94 | 197,098 | 930 | 24.44 | 63,378 | 4.4 | 33% | 102,569 | 4.7% | -0.84% | 182 |

| 93 | Columbia, SC | 9.2 | 0.00% | 856.3 | 6.90% | 2.4 | 14.60% | 102 | 5,480 | 987 | 23.70% | 10 | -55% | 43,994 | 1.45 | 52,332 | 1.76 | 208,249 | 811 | 10.61 | 47,314 | 4.2 | 31% | 63,933 | 3.0% | 4.00% | 92 |

| 94 | Manchester-Nashua, NH | 9 | 1.70% | 703 | 5.60% | 2.5 | 8.20% | 203 | 1,382 | 866 | 8.50% | 12 | -66% | 2,944 | 1.68 | 8,507 | 3.37 | 107,074 | 390 | 19.7 | 44,224 | 8.8 | 43% | 96,921 | 2.4% | -0.17% | 116 |

| 95 | Nashville-Davidson--Murfreesboro--Franklin, TN | 9.7 | 1.20% | 684.2 | 16.50% | 2.4 | 25.50% | 141 | 23,903 | 922 | 26.80% | 8 | -24% | 31,927 | 0.41 | 88,874 | 0.44 | 534,771 | 1,832 | 7.08 | 209,760 | 1.2 | 54% | 80,034 | 2.7% | 2.38% | 108 |

| 96 | Flint, MI | 8.2 | 5.40% | 1,064.60 | -3.20% | 2.4 | 2.60% | 289 | 393 | 874 | 11.80% | 7 | -30% | 9,852 | 1.08 | 13,723 | 4.12 | 92,417 | 752 | 13.02 | 20,430 | 10 | 38% | 57,003 | 4.9% | 3.86% | 84 |

| 97 | Fresno, CA | 7.5 | 3.40% | 259.1 | 6.30% | 3 | 11.40% | 43 | 3,223 | 899 | 22.30% | 9 | -41% | 12,810 | 0.77 | 70,108 | 1.48 | 206,680 | 1,275 | 8.09 | 49,340 | 3.9 | 58% | 69,571 | 8.0% | -0.88% | 122 |

| 98 | Visalia, CA | 7.4 | 2.30% | 300 | 5.20% | 3.3 | 7.30% | 32 | 1,175 | 891 | 23.40% | 9 | -30% | 10,514 | 0.78 | 19,548 | 3.13 | 98,113 | 502 | 6.85 | 10,375 | 9 | 64% | 64,722 | 10.9% | -0.99% | 105 |

| 99 | Modesto, CA | 8.6 | 0.00% | 385.1 | 4.90% | 3.1 | 5.80% | 123 | 805 | 791 | 39.00% | 9 | -49% | 7,775 | 1.27 | 26,934 | 2.82 | 123,907 | 609 | 6.76 | 16,921 | 6.9 | 58% | 75,886 | 6.9% | -0.04% | 115 |

| 100 | Louisville, KY-IN | 8.5 | 1.50% | 808.2 | 1.80% | 2.4 | 8.40% | 144 | 6,810 | 916 | 23.10% | 8 | -44% | 15,690 | 0.4 | 50,462 | 1.41 | 317,376 | 1,059 | 812.45 | 87,748 | 2.4 | 37% | 69,547 | 3.9% | -1.56% | 86 |

| 101 | Austin-Round Rock-Georgetown, TX | 10.4 | 2.30% | 457.3 | 28.60% | 2.4 | 45.20% | 248 | 38,599 | 879 | 51.90% | 6 | 16% | 35,858 | 0.43 | 137,160 | 0.95 | 593,446 | 3,584 | 14.86 | 374,610 | 1.2 | 53% | 94,604 | 3.4% | 3.13% | 103 |

| 102 | Boise City, ID | 15.9 | 5.90% | 1,655.30 | 25.30% | 2.6 | 29.50% | 27 | 9,882 | 883 | 42.10% | 10 | -44% | 14,922 | 1.19 | 39,749 | 2.87 | 219,832 | 1,046 | 16.85 | 68,016 | 6.3 | 63% | 80,928 | 3.3% | 2.54% | 98 |

| 103 | Virginia Beach-Norfolk-Newport News, VA-NC | 10.2 | 1.20% | 858.6 | 5.90% | 2.5 | 14.50% | 241 | 6,114 | 924 | 25.90% | 10 | -59% | 17,581 | 1.59 | 100,931 | 1.84 | 435,481 | 1,097 | 24.02 | 100,526 | 5.8 | 33% | 74,556 | 3.0% | 2.41% | 104 |

| 104 | Houston-The Woodlands-Sugar Land, TX | 10.9 | 1.70% | 668.8 | 16.30% | 2.7 | 24.30% | 327 | 68,336 | 889 | 43.10% | 7 | -27% | 126,612 | 0.27 | 301,604 | 1.38 | 1,640,264 | 11,257 | 18.11 | 458,353 | 1.3 | 31% | 74,863 | 4.2% | 2.82% | 91 |

| 105 | Ogden-Clearfield, UT | 11.6 | 3.70% | 1,035.80 | 15.00% | 3 | 20.70% | 161 | 3,323 | 883 | 34.20% | 9 | -8% | 6,287 | 1.14 | 30,137 | 2.73 | 177,447 | 1,151 | 13.44 | 65,483 | 5.8 | 47% | 92,600 | 2.8% | 2.75% | 104 |

| 106 | Savannah, GA | 9.9 | 3.40% | 1,061.70 | 14.30% | 2.5 | 23.40% | 135 | 3,408 | 969 | 25.50% | 10 | -53% | 10,556 | 1.43 | 31,430 | 1.75 | 101,531 | 520 | 11.19 | 22,796 | 4.2 | 47% | 72,098 | 2.8% | 2.02% | 121 |

| 107 | North Port-Sarasota-Bradenton, FL | 10.5 | 10.60% | 992.1 | 21.70% | 2.2 | 29.50% | 375 | 15,919 | 944 | 25.80% | 9 | -36% | 51,762 | 1.08 | 11,299 | 1.69 | 215,624 | 1,174 | 14.51 | 65,500 | 3.7 | 57% | 75,631 | 3.3% | 2.42% | 118 |

| 108 | Tulsa, OK | 11.2 | 0.40% | 1,702.20 | 7.50% | 2.5 | 10.50% | 71 | 5,111 | 826 | 30.50% | 9 | -45% | 26,842 | 0.84 | 33,348 | 1.68 | 251,004 | 1,683 | 8.18 | 50,961 | 5.2 | 31% | 63,396 | 3.6% | 4.77% | 82 |

| 109 | Asheville, NC | 10.7 | 2.40% | 1,166.40 | 8.80% | 2.4 | 4.50% | 162 | 3,831 | 951 | 21.10% | 12 | -24% | 31,141 | 0.93 | 16,404 | 3.24 | 119,404 | 189 | 14.51 | 33,876 | 7.6 | 50% | 66,023 | 2.8% | 1.72% | 94 |

| 110 | Omaha-Council Bluffs, NE-IA | 8.9 | 0.00% | 367.9 | 9.00% | 2.4 | 14.40% | 95 | 4,705 | 907 | 22.20% | 12 | -50% | 4,019 | 0.41 | 64,023 | 1.13 | 245,326 | 851 | 5.36 | 74,699 | 2.7 | 44% | 79,638 | 2.7% | -0.22% | 85 |

| 111 | Knoxville, TN | 9.3 | 3.10% | 968 | 6.40% | 2.4 | 8.70% | 116 | 6,380 | 915 | 9.60% | 15 | -56% | 33,087 | 0.92 | 55,192 | 1.33 | 243,257 | 850 | 5.55 | 56,060 | 3.4 | 50% | 67,801 | 3.1% | 2.44% | 106 |

| 112 | Las Vegas-Henderson-Paradise, NV | 9.6 | 2.40% | 422.2 | 14.60% | 2.7 | 20.10% | 120 | 13,073 | 891 | 55.60% | 8 | -28% | 28,063 | 0.5 | 75,458 | 0.86 | 474,870 | 3,207 | 16.36 | 142,376 | 1.4 | 39% | 70,797 | 5.4% | 4.27% | 114 |

| 113 | Huntsville, AL | 13.4 | 3.30% | 1,151.60 | 18.10% | 2.4 | 21.50% | 164 | 5,943 | 943 | 22.70% | 6 | -42% | 9,781 | 2.16 | 28,839 | 3.09 | 132,241 | 716 | 11.13 | 36,347 | 8 | 45% | 81,066 | 2.4% | 2.76% | 74 |

| 114 | Pensacola-Ferry Pass-Brent, FL | 11.2 | 2.40% | 1,252.30 | 12.00% | 2.4 | 20.10% | 138 | 2,824 | 953 | 32.90% | 5 | -24% | 16,471 | 1.27 | 22,128 | 3.02 | 124,347 | 749 | 14.94 | 36,534 | 8.1 | 44% | 68,034 | 3.2% | 1.80% | 83 |

| 115 | Lexington-Fayette, KY | 8.8 | 0.60% | 573.5 | 5.80% | 2.3 | 12.30% | 157 | 2,365 | 876 | 20.60% | 8 | -57% | 6,234 | 0.69 | 51,655 | 2.43 | 124,435 | 428 | 6.94 | 29,841 | 5.9 | 31% | 65,964 | 3.6% | -0.38% | 98 |

| 116 | Spokane-Spokane Valley, WA | 12.1 | 1.30% | 1,238.30 | 11.70% | 2.4 | 15.20% | 60 | 3,904 | 867 | 29.00% | 11 | -46% | 13,521 | 1.5 | 31,385 | 2.04 | 152,857 | 969 | 18.67 | 44,004 | 5 | 45% | 68,829 | 4.6% | 1.03% | 109 |

| 117 | Eugene-Springfield, OR | 10.2 | 7.70% | 1,402.40 | 7.30% | 2.3 | 11.20% | 37 | 1,239 | 859 | 18.20% | 8 | -32% | 13,155 | 2.51 | 30,645 | 3.61 | 89,788 | 258 | 11.29 | 27,544 | 7.8 | 47% | 64,069 | 4.3% | -0.43% | 124 |

| 118 | San Antonio-New Braunfels, TX | 10.2 | 4.20% | 466.4 | 16.60% | 2.7 | 24.90% | 145 | 16,519 | 858 | 55.00% | 6 | -7% | 53,843 | 0.42 | 135,592 | 0.77 | 595,837 | 3,605 | 8.99 | 189,650 | 1.6 | 36% | 70,538 | 3.6% | 2.68% | 104 |

| 119 | Dallas-Fort Worth-Arlington, TX | 10.5 | 2.40% | 394.4 | 16.60% | 2.7 | 20.90% | 357 | 66,557 | 873 | 48.80% | 8 | -31% | 97,884 | 0.18 | 358,235 | 0.67 | 1,821,991 | 12,261 | 10.24 | 745,593 | 0.9 | 44% | 82,823 | 3.7% | 2.68% | 98 |

| 120 | Sacramento-Roseville-Folsom, CA | 8.9 | 5.30% | 209.1 | 9.10% | 2.7 | 11.60% | 188 | 11,917 | 847 | 42.50% | 10 | -46% | 28,934 | 0.23 | 168,405 | 0.43 | 565,949 | 3,374 | 7.83 | 225,416 | 0.8 | 56% | 89,237 | 4.7% | -0.39% | 135 |

| 121 | Fayetteville-Springdale-Rogers, AR | 17 | 4.60% | 1,181.80 | 17.30% | 2.6 | 21.70% | 90 | 6,865 | 892 | 11.30% | 12 | -53% | 12,877 | 1.32 | 41,012 | 3.03 | 141,357 | 361 | 6.46 | 39,644 | 7 | 53% | 73,364 | 2.5% | 1.64% | 73 |

| 122 | Chattanooga, TN-GA | 9.8 | 6.50% | 1,172.80 | 6.20% | 2.4 | 10.40% | 122 | 3,011 | 919 | 22.80% | 8 | -31% | 15,078 | 0.86 | 24,542 | 1.9 | 150,500 | 399 | 10.09 | 39,725 | 4.7 | 45% | 69,018 | 3.1% | 2.35% | 80 |

| 123 | Bakersfield, CA | 8.9 | 2.10% | 296.4 | 6.00% | 3.1 | 10.20% | 38 | 2,462 | 863 | 16.30% | 9 | -31% | 24,503 | 0.74 | 47,173 | 2.21 | 185,487 | 1,576 | 9.8 | 25,409 | 5.4 | 41% | 66,234 | 8.8% | -1.14% | 96 |

| 124 | New Orleans-Metairie, LA | 8.8 | 1.10% | 468.6 | 0.40% | 2.5 | 4.30% | 246 | 3,101 | 842 | 14.00% | 7 | 11% | 22,363 | 0.65 | 57,370 | 0.73 | 256,838 | 886 | 13.64 | 64,876 | 1.8 | 34% | 61,602 | 4.1% | -1.28% | 110 |

| 125 | Augusta-Richmond County, GA-SC | 11 | 0.60% | 1,002.70 | 7.10% | 2.6 | 13.80% | 78 | 3,550 | 932 | 25.70% | 7 | -49% | 37,908 | 0.95 | 19,863 | 3.13 | 142,403 | 961 | 8.15 | 27,800 | 7.7 | 46% | 64,581 | 3.7% | 0.94% | 90 |

| 126 | Crestview-Fort Walton Beach-Destin, FL | 15.6 | 3.60% | 1,092.00 | 18.20% | 2.4 | 25.90% | 84 | 5,596 | 952 | 30.10% | 5 | -14% | 13,078 | 1.51 | 4,898 | 4.53 | 81,930 | 358 | 10.78 | 15,805 | 10.1 | 45% | 76,945 | 2.8% | 2.21% | 116 |

| 127 | Fayetteville, NC | 11 | 7.80% | 857 | 40.30% | 2.5 | 41.70% | 210 | 2,547 | 998 | 48.70% | 8 | -63% | 23,566 | 1.03 | 24,728 | 2.95 | 125,001 | 177 | 9.01 | 18,629 | 7.5 | 41% | 60,441 | 4.6% | 2.07% | 93 |

| 128 | Baton Rouge, LA | 11.8 | 0.40% | 1,158.70 | 6.50% | 2.5 | 12.00% | 88 | 3,272 | 939 | 22.60% | 4 | -53% | 41,262 | 2.09 | 59,858 | 2.42 | 197,890 | 944 | 41.8 | 30,924 | 5.6 | 26% | 64,222 | 3.6% | -0.64% | 87 |

| 129 | Albuquerque, NM | 8.9 | 4.60% | 527.3 | 2.40% | 2.4 | 12.70% | 43 | 2,977 | 811 | 48.60% | 9 | -58% | 30,394 | 0.71 | 44,865 | 1.22 | 225,393 | 1,367 | 9.29 | 64,381 | 3.9 | 37% | 66,392 | 3.7% | 1.67% | 98 |

| 130 | Sioux Falls, SD | 11.9 | 0.00% | 504.7 | 18.70% | 2.4 | 26.30% | 40 | 3,448 | 887 | 5.10% | 9 | -50% | 4,285 | 0.91 | 7,050 | 3.34 | 76,739 | 214 | 7.59 | 18,648 | 7.7 | 39% | 77,605 | 1.8% | 2.26% | 91 |

| 131 | Cape Coral-Fort Myers, FL | 10.5 | 11.20% | 598.7 | 24.40% | 2.4 | 40.60% | 566 | 13,556 | 975 | 21.90% | 9 | 9% | 37,025 | 0.45 | 31,338 | 1.05 | 184,496 | 907 | 10.69 | 53,495 | 2.1 | 53% | 71,072 | 3.2% | 1.43% | 113 |

| 132 | Naples-Marco Island, FL | 11.4 | 3.50% | 835.8 | 17.20% | 2.4 | 27.20% | 120 | 3,633 | 1,004 | 14.00% | 9 | -50% | 10,869 | 0.78 | 1,575 | 2.95 | 91,361 | 483 | 18.29 | 26,502 | 7.4 | 49% | 80,815 | 3.1% | 2.20% | 133 |

| 133 | Killeen-Temple, TX | 12.3 | 6.70% | 588.9 | 17.20% | 2.6 | 35.50% | 69 | 3,523 | 821 | 40.70% | 9 | 34% | 14,298 | 1.85 | 18,701 | 3.24 | 112,293 | 840 | 14.66 | 24,425 | 7.1 | 25% | 62,904 | 4.3% | 1.50% | 90 |

| 134 | Greensboro-High Point, NC | 9.2 | 6.30% | 802.3 | 5.80% | 2.4 | 10.20% | 173 | 3,493 | 933 | 37.70% | 8 | -45% | 24,901 | 0.9 | 56,980 | 2.07 | 198,838 | 478 | 8.54 | 45,330 | 4.9 | 38% | 60,271 | 3.9% | 1.01% | 91 |

| 135 | Santa Rosa-Petaluma, CA | 9.8 | 5.10% | 750.5 | -2.50% | 2.4 | 3.00% | 132 | 2,353 | 826 | 39.80% | 7 | -44% | 9,731 | 1.75 | 22,486 | 3.67 | 125,283 | 428 | 12.59 | 35,126 | 8.4 | 59% | 96,830 | 4.0% | -0.64% | 182 |

| 136 | Oklahoma City, OK | 12.5 | 1.30% | 585.5 | 10.60% | 2.5 | 15.50% | 113 | 6,458 | 844 | 17.80% | 6 | -37% | 30,175 | 0.54 | 80,988 | 0.96 | 348,959 | 2,882 | 11.92 | 75,686 | 2.4 | 32% | 66,301 | 3.3% | 4.15% | 77 |

| 137 | Reno, NV | 15.3 | 0.20% | 453.1 | 14.20% | 2.5 | 20.40% | 26 | 4,271 | 853 | 40.50% | 7 | -34% | 12,276 | 1.33 | 31,351 | 2.93 | 127,654 | 825 | 12.37 | 27,250 | 6.9 | 49% | 80,333 | 4.1% | 1.99% | 119 |

| 138 | Wilmington, NC | 14.4 | 4.10% | 1,232.80 | 11.90% | 2.3 | 21.70% | 79 | 3,829 | 957 | 32.10% | 6 | -58% | 7,866 | 1.65 | 32,530 | 3.8 | 80,925 | 549 | 9.9 | 27,859 | 8.4 | 52% | 72,339 | 3.2% | 0.90% | 100 |

| 139 | Waco, TX | 13.5 | 0.00% | 426.9 | 10.00% | 2.7 | 8.10% | 42 | 1,741 | 864 | 23.80% | 9 | 15% | 7,089 | 1.41 | 38,252 | 4.92 | 62,851 | 540 | 8.9 | 13,863 | 11.5 | 58% | 63,501 | 3.6% | 2.20% | 93 |

| 140 | Columbus, GA-AL | 11.9 | 0.00% | 1,103.30 | 3.10% | 2.5 | 13.60% | 52 | 647 | 1,052 | 43.80% | 7 | -53% | 9,979 | 1.51 | 12,554 | 3.63 | 70,537 | 231 | 10.89 | 16,815 | 7.9 | 34% | 54,106 | 3.6% | 0.75% | 92 |

| 141 | Tallahassee, FL | 11 | 2.60% | 943.3 | 4.70% | 2.3 | 9.10% | 75 | 2,694 | 1,024 | 21.90% | 6 | -53% | 23,958 | 3.28 | 64,642 | 2.95 | 86,547 | 142 | 6.07 | 17,732 | 7.5 | 31% | 58,018 | 3.3% | 2.31% | 100 |

| 142 | Birmingham-Hoover, AL | 9 | 1.30% | 453.6 | -2.10% | 2.5 | 2.90% | 94 | 3,287 | 969 | 28.10% | 5 | -39% | 37,179 | 0.56 | 45,829 | 0.58 | 280,174 | 800 | 4.67 | 62,270 | 1.4 | 39% | 67,242 | 2.6% | 1.27% | 92 |

| 143 | San Luis Obispo-Paso Robles, CA | 12.8 | 0.00% | 516.3 | 2.00% | 2.4 | 6.70% | 38 | 997 | 841 | 18.20% | 13 | -55% | 8,612 | 0.81 | 32,549 | 3.79 | 73,187 | 413 | 10.03 | 21,445 | 13.3 | 55% | 90,216 | 3.8% | -0.97% | 155 |

| 144 | Memphis, TN-MS-AR | 9.9 | 1.50% | 451.9 | -1.00% | 2.5 | 5.40% | 115 | 4,104 | 918 | 28.70% | 8 | -22% | 23,099 | 0.79 | 52,023 | 1.02 | 309,787 | 2,240 | 6.65 | 68,923 | 2.8 | 36% | 64,008 | 3.9% | -0.37% | 87 |

| 145 | Mobile, AL | 10.6 | 0.50% | 389.6 | 3.60% | 2.5 | 14.10% | 158 | 905 | 907 | 23.40% | 7 | -41% | 15,713 | 0.69 | 19,511 | 1.69 | 100,988 | 434 | 3.77 | 14,694 | 3.7 | 26% | 54,313 | 3.7% | -0.23% | 84 |

| 146 | Lubbock, TX | 16.7 | 1.90% | 453 | 7.70% | 2.4 | 19.80% | 28 | 2,514 | 913 | 22.80% | 4 | -21% | 7,170 | 2.29 | 47,110 | 3.14 | 78,498 | 1,306 | 5 | 9,993 | 7.1 | 26% | 59,228 | 3.3% | 1.74% | 84 |

| 147 | Little Rock-North Little Rock-Conway, AR | 12.6 | 8.10% | 590.3 | 4.70% | 2.4 | 17.10% | 84 | 2,655 | 869 | 28.10% | 8 | -49% | 30,973 | 0.44 | 35,191 | 0.87 | 182,969 | 985 | 5.11 | 35,344 | 2.6 | 26% | 60,931 | 3.2% | 1.76% | 76 |

| 148 | Corpus Christi, TX | 13.7 | 4.60% | 576.7 | -5.20% | 2.6 | -2.60% | 104 | 1,790 | 860 | 41.70% | 5 | -32% | 9,644 | 0.84 | 20,503 | 3.69 | 88,703 | 562 | 8.38 | 9,404 | 8.5 | 26% | 61,169 | 4.2% | 2.72% | 95 |

| 149 | Jackson, MS | 11.5 | 0.00% | 209.9 | 0.40% | 2.5 | 8.20% | 43 | 1,220 | 934 | 32.80% | 6 | -38% | 27,211 | 0.17 | 33,455 | 1.72 | 135,454 | 406 | 3.2 | 18,914 | 1.8 | 33% | 58,064 | 2.7% | 0.34% | 89 |

| 150 | Lafayette, LA | 13.9 | 3.50% | 521.7 | 0.40% | 2.5 | 8.70% | 77 | 2,389 | 899 | 5.40% | 6 | -65% | 35,704 | 0.61 | 24,432 | 1.52 | 105,430 | 99 | 9.29 | 16,645 | 4.6 | 6% | 50,837 | 3.9% | -1.02% | 74 |

RentCafe analysis of data from the U.S. Census, Yardi Matrix, National Center for Education Statistics, Google Ads Keyword Planner, RentCafe, Zillow and the U.S. Bureau of Labor Statistics

Methodology:

This analysis was done by RentCafe Self Storage, an online platform that provides apartment and storage unit listings nationwide.

The scope of this study was to identify the markets with the highest potential for further self storage development, as expressed by the relationship between the existing inventory and the local demand drivers. To do so, we analyzed the country’s largest 150 metro areas based on a wide set of 25 metrics, including self storage market conditions, demographic factors, housing market, additional sources of demand and the local economy.

The complete list of metrics and weightings is below:

For the purpose of this study, the markets we analyzed were classified as primary, secondary and tertiary markets. Primary markets are the metro areas with a population of 5-plus million, secondary markets have a population of 2 million to 5 million, and tertiary markets have a population of under 2 million.

Fair use and redistribution

We encourage you and freely grant you permission to reuse, host or repost the research, graphics and images presented in this article. When doing so, we ask that you credit our research by linking to RentCafe Self Storage or to this page.

Share this article:

Maria Gatea

Maria Gatea is a Senior Editor & Research Writer for Yardi with a background in Journalism and Communication. After covering business and finance-related topics as a freelance writer for 15 years, she is now focusing on researching and writing about the real estate industry. You may contact Maria via email.

Sign up for The Ready Renter newsletter

Get our free apartment hunting guide — plus tips, trends, and research.

")

")

Related posts

Green flags vs. red flags: what to notice on every apartment tour

Finding a place online is the easy part. The apartment tour is where you find out what the photos left out. For a first-time renter,…

Renting like a local: 5 questions to ask before signing a lease in Boston

Boston is one of the most rewarding cities to call home. It’s walkable, full of history and packed with distinct neighborhoods that each have their…

Here’s how to get around Pittsburgh as a renter using public transit

Pittsburgh is a city of three rivers, steep ridges and nearly 450 bridges. All that terrain shapes how you get from your front door to…

Subscribe to

The Ready Renter newsletter