Survey: Cost Barrier Keeps Over 80 Percent of Renters Away from Their Ideal Location, Their Job

Share this article:

Job growth in and near downtown areas is seeing peak levels, with major employers like McDonald’s in Chicago and GE in Boston relocating their headquarters from the suburbs to the city cores to have direct access to young intellectual capital and to attract tech-savvy Millennial talent. Such changes are forging a stronger bond between jobs and residential and commercial development. But in spite of the construction boom, not everyone can afford to live in an ideal location, close to where the jobs are, and especially not Millennial renters.

Less than 17% of over 2,000 renters we recently surveyed said they live close to their ideal location, leaving 83% of renters living in less than ideal locations, and the cost of rent was listed as their no. 1 concern. Our survey also found that the ‘ideal location’ for most renters is near their job, ahead of living close to friends and family, or near attractions such as entertainment, dining, shopping or a gym. Moreover, 60% of respondents stated that they are not able to pay anything more than the rent they are already paying (16.4% of respondents) or a maximum of $100 more (43.2% of respondents) to live in their preferred location. This reality rings true especially for Millennials, who make up over 70% of our survey respondents.

A location upgrade costs over 4 times as much as what most renters are willing to pay

An ideal location typically refers to apartments in or near central neighborhoods (although not always), which also happen to overlap with most cities’ central business districts with high concentrations of jobs, as well as more entertainment, shopping, and dining within walking distance. But the cost of land tends to be high in those locations, which drags up the price of rent. Nationally, the average rent charged by buildings in top-rated locations is $1,655/month, 37% more than the national average rent of $1,211 charged in lower-rated locations, a difference of $444 per month, according to rent data and location ratings by Yardi Matrix. Based on the survey responses illustrated above, the percentage of renters who can afford the price of a location upgrade is very very low.

The $444 rent gap comes from comparing average rents in apartments in top-notch locations rated A+/A/A-/B+ and apartments in average and below-average locations rated B/B-/C/D. Some of the attributes that earn a property location top ratings are close proximity to a high concentration of good employment sources, high-quality mix of immediate area housing, shopping, and entertainment, and ease of access. Among the attributes that lower a location’s rating are a low availability of quality area employment, limited or deteriorated commercial development in the area, and inconvenient access.

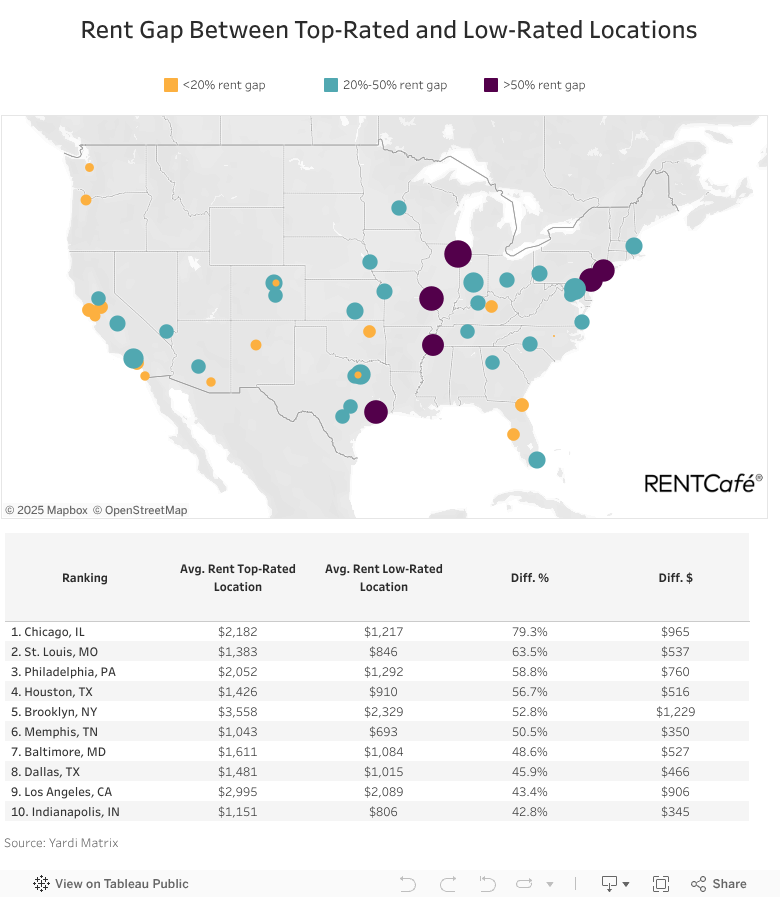

In Chicago and 5 other cities renters pay over 50% more for their ideal location

On the map above, the largest circles indicate the largest percentage difference in the average price between a rental in a top location versus a rental in a less desirable location. The six dark purple dots are cities where this difference is higher than 50%: Chicago, St. Louis, Philadelphia, Houston, Brooklyn, NYC, and Memphis.

Jobs in downtown Chicago have surged in 2017 and apartment development in the area is booming, including giant projects like the 1,400-foot tall Tribune Tower in the plans. But centrally-located Chicago apartments cost on average 79% more than apartments in other neighborhoods further out. The average renter is looking at almost $1,000 extra per month to rent an apartment in a top-notch location in the city of Chicago, which adds up to $12,000 extra in rent/year. The average rent for an apartment in one of the best locations in the city is $2,182/month, while the average rent for an apartment in a second-rate location is $1,217/month. Top Chicago locations are mostly areas in and around downtown, clustered in the area bordered by Roosevelt Road to the South, Racine Ave. to the West and W. Addison St. to the North, according to Yardi Matrix location data.

One would probably have to do a case study for each individual city to pinpoint the exact mix of factors that contribute to the price of rent in different locations. Part of the mix are the availability of apartments in the different neighborhoods, the strength of the local job market, the geography of jobs, the demand for rental apartments, and the public transportation system, among other local factors.

In St. Louis, MO, for instance, the low-availability of rentals in good locations is one of the main reasons there is a stark 63.5% price gap between rentals in top-rated and low-rated locations, the second highest on our list. The average rent in a top St. Louis location is $1,383/month, while the rent in an average or below average location costs $846/month.

Philadelphia has the third largest rent gap between top-rated and low-rated locations, with rents in highly-rated locations 59% more expensive. Center City holds 42% of jobs in Philadelphia, the largest employment hub in the city and the region. With companies like Comcast, the largest employer in Philadelphia, extending its offices in Center City to make room for more employees, the demand for centrally-located rental housing is increasing. But the prospect of those who work in the heart of Philly to also live in it is unlikely as long as the average rent is a whopping $2,052 per month, $760 more than an apartment in other lower-rated neighborhoods.

Renters in Houston in search of a better location are looking at a 57% rent gap, fourth on the list. Apartments in lower-rated locations in Houston cost on average $910/month, jumping to $1,426 for an apartment in a top-notch location. Brooklyn renters would also have to raise their budget by 53% if they wanted to live in a great location. The cost of rent in an average or below-average location in Brooklyn, NYC is $2,329/month, compared to an average of $3,558/month in a first-rate location.

Other notable cities are Baltimore, MD; Dallas, TX; Los Angeles, CA; Indianapolis, IN; Miami, FL; Wichita, KS; Boston, MA; Denver, CO; Fresno, CA; Kansas City, MO; Pittsburgh, PA; Charlotte, NC; Fort Worth, TX; Columbus, OH; Virginia Beach, VA; Omaha, NE; Minneapolis, MN; Louisville, KY; Las Vegas, NV; Atlanta, GA; Phoenix, AZ; Colorado Springs, CO; San Antonio, TX; Nashville, TN; Austin, TX; Sacramento, CA; Washington, DC; Stockton, CA; San Francisco, CA; Jacksonville, FL; Santa Ana, CA; Tulsa, OK; Lexington, KY; Tampa, FL; Albuquerque, NM; Manhattan, NY; San Jose, CA and Portland, OR.

Raleigh and Seattle among the 6 cities where renters pay less than 10% more for a top location

Downtown living is less of a stretch for renters in Raleigh, NC, Aurora, CO, Arlington, TX, Seattle, WA, San Diego, CA and Tucson, AZ, where the rent budget would need an increase of only 10% or less for a location upgrade. This surprisingly even price distribution has to do with various local economic factors. It often depends on whether there are enough highly-paid jobs in a certain city to sustain a strong demand for high-priced apartments. If that demand is not strong enough, prices tend to adjust accordingly. This may be the case in Tucson, AZ where the employment mix makes for a median income well below the national average. On the other hand, in strong job markets like Seattle and San Diego, rents are high in most locations, even lower-rated ones, thanks to the competitiveness of the housing market.

In Raleigh, the city with the smallest location rent gap, the housing market has managed to remain somewhat quiet, in the midst of a national housing ruckus. The average rent in Raleigh is well below the national average ($1,381), and prices for apartments in the city’s top locations are virtually the same as those in lower-rated locations. ($1,109/month vs $1,107/month). But things might soon change for Raleigh (more recently nicknamed “Boomtown, USA”), as job growth over the next 10 years is predicted to be 42%, according to MarketWatch.

Similarly, the rent in Aurora, CO doesn’t change significantly from a top location to other lower-rated locations. One can easily make the move to a better location for an additional $67/month or 5% in rent ($1,250 vs $1,317), the second narrowest rent gap. In Arlington, TX the price of apartments in the best locations is 6% higher ($56 more per month) than apartments in average and below average locations. The difference in rent for apartments in good vs bad locations is 8.4% in Seattle, 8.7% in San Diego, and 9.6% in Tucson.

Location preferences change with age, the survey showed

The ideal location changes with age. Our renter survey also showed that younger, working generations are mostly interested in living closer to work, while older, retired generations prioritize being close to friends and family. The third most popular location choice is proximity to entertainment, dining, shopping or gym, at a time when walkability is highly valued by renters of all ages. 17% of millennials, 19% of Gen-X-ers, 20% of Baby-Boomers, and 20% of the Silent generation chose this as their preferred location. Being close to school is also important for those with young children. In fact, for renters who said they would be willing to pay $250 extra for a better location, their top-priority location was proximity to good schools.

A clear majority of Generation Z renters (64%) want to live close to work/university, with other types of locations being of secondary importance. For almost 30% of Millennials, work/university is the first choice of location, the same as for 27% of Generation X-ers. As far as retirees go, 34% of Baby-Boomer renters picked being close to friends and family as the most important location criteria, while for the Silent Generation, proximity to friends and family and public transportation are equally important.

Rents in top locations are higher, but increase slower

With so many new apartment buildings crowding the skylines, many renters are kicking the tires in attractive locations in hopes of a price reduction in the foreseeable future. But their wishes remain unanswered. All they’re seeing, for now, are more subdued increases in rents in those much-coveted locations compared to bolder increases in low-budget apartments in average and below-average locations.

Yardi Matrix rent data reinforces that, in the last 3 years, the cost of rent in first-rate locations grew slower than in lower-rated locations. However, the reason is not necessarily the overbuilding in urban cores, as some may argue. Interestingly enough, since 2015, in the 50 cities analyzed, more apartments were built in low-rated locations. In total, about 207,000 apartments (54%) were completed in lower-rated locations, and 173,000 apartments (46%) were completed in highly-rated locations, although these numbers include only large-scale buildings of 50 or more units. Higher increases in rents are the result of higher demand for apartments in less-desirable locations, where prices are lower, which is what most renters are after.

What’s expected for the future

With the current shifting of highly-skilled jobs closer to city cores, urban infill in highly-coveted ideal locations is yet to reach its full potential. In fact, judging by the number of projects under construction, top locations are building fewer apartment developments than other locations. The 50 cities analyzed have a combined 105,000 apartments under construction (40%) in best-rated locations and 158,000 apartments under construction (60%) in lower-rated locations. As rental development in walkable urban areas is underway, we expect prices to approach more affordable levels as a natural next step in this process that the Brookings Institute calls “catalytic development“.

| Largest 50 cities | Diff. % | Diff. $ | AverageRent Top-Rate Location | AverageRent Low-Rate Location |

|---|---|---|---|---|

| Chicago, IL | 79.3% | $965 | $2,182 | $1,217 |

| St. Louis, MO | 63.5% | $537 | $1,383 | $846 |

| Philadelphia, PA | 58.8% | $760 | $2,052 | $1,292 |

| Houston, TX | 56.7% | $516 | $1,426 | $910 |

| Brooklyn, NY | 52.8% | $1,229 | $3,558 | $2,329 |

| Memphis, TN | 50.5% | $350 | $1,043 | $693 |

| Baltimore, MD | 48.6% | $527 | $1,611 | $1,084 |

| Dallas, TX | 45.9% | $466 | $1,481 | $1,015 |

| Los Angeles,CA | 43.4% | $906 | $2,995 | $2,089 |

| Indianapolis, IN | 42.8% | $345 | $1,151 | $806 |

| Miami, FL | 33.6% | $509 | $2,024 | $1,515 |

| Wichita, KS | 30.9% | $190 | $804 | $614 |

| Boston, MA | 30.8% | $802 | $3,407 | $2,605 |

| Denver, CO | 30.6% | $433 | $1,849 | $1,416 |

| Fresno, CA | 29.1% | $270 | $1,198 | $928 |

| Kansas City, MO | 27.9% | $251 | $1,150 | $899 |

| Pittsburgh, PA | 27.2% | $307 | $1,434 | $1,127 |

| Charlotte, NC | 26.2% | $285 | $1,374 | $1,089 |

| Fort Worth, TX | 25.5% | $246 | $1,210 | $964 |

| Columbus, OH | 25.1% | $219 | $1,090 | $871 |

| Virginia Beach, VA | 24.8% | $276 | $1,390 | $1,114 |

| Omaha, NE | 24.8% | $208 | $1,048 | $840 |

| Minneapolis, MN | 24.7% | $347 | $1,750 | $1,403 |

| Louisville, KY | 24.4% | $210 | $1,071 | $861 |

| Las Vegas, NV | 23.5% | $220 | $1,157 | $937 |

| Atlanta, GA | 23.3% | $283 | $1,499 | $1,216 |

| Phoenix, AZ | 23.0% | $212 | $1,135 | $923 |

| Colorado Springs, CO | 22.8% | $226 | $1,219 | $993 |

| San Antonio, TX | 22.2% | $205 | $1,127 | $922 |

| Nashville, TN | 21.9% | $275 | $1,533 | $1,258 |

| Austin, TX | 21.2% | $248 | $1,418 | $1,170 |

| Sacramento, CA | 20.8% | $257 | $1,491 | $1,234 |

| Washington, DC | 20.1% | $370 | $2,208 | $1,838 |

| Stockton, CA | 19.7% | $205 | $1,248 | $1,043 |

| San Francisco, CA | 19.5% | $590 | $3,622 | $3,032 |

| Jacksonville, FL | 19.2% | $180 | $1,119 | $939 |

| Santa Ana, CA | 18.1% | $309 | $2,017 | $1,708 |

| Tulsa, OK | 16.9% | $110 | $759 | $649 |

| Lexington, KY | 16.0% | $138 | $1,003 | $865 |

| Tampa, FL | 15.5% | $186 | $1,383 | $1,197 |

| Albuquerque, NM | 13.6% | $108 | $904 | $796 |

| Manhattan, NY | 13.5% | $491 | $4,134 | $3,643 |

| San Jose, CA | 12.8% | $319 | $2,804 | $2,485 |

| Portland, OR | 12.8% | $176 | $1,551 | $1,375 |

| Tucson, AZ | 9.6% | $75 | $860 | $785 |

| San Diego, CA | 8.7% | $173 | $2,158 | $1,985 |

| Seattle, WA | 8.4% | $162 | $2,084 | $1,922 |

| Arlington, TX | 5.8% | $56 | $1,017 | $961 |

| Aurora, CO | 5.4% | $67 | $1,317 | $1,250 |

| Raleigh, NC | 0.2% | $2 | $1,109 | $1,107 |

Methodology

For this study, we surveyed 2,015 U.S. renters nationwide via Amazon’s Mechanical Turk. The respondents were asked individual questions about their rental preferences and some demographic data such as age, income, and city. Our survey sample size has a 3% margin of error and a 99% confidence level.

Apartment community location ratings are as defined by Yardi Matrix. Apartment data comes from large-scale properties of 50 units or more. We considered top-rated locations (also referred to as “good locations”) all rental apartment buildings that received location ratings of A+/A/A-/B+ and low-rated locations (also referred to as “average and below-average locations”) those rated B/B-/C/C-/D.

Average rents are as of March 2018 and come from apartment communities of 50 or more units. Rents from affordable housing were not included.

The cities included in this study have a minimum population of 100,000 and at least 2,000 apartment units in each category (top-rated locations and low-rated locations). The study covers a total of 50 U.S. cities.

Share this article:

Nadia Balint

Nadia Balint is a senior creative writer for RENTCafé. She covers news and trends in residential and commercial real estate and their impact on our everyday life, including rental housing, for-sale housing, real estate development, homeownership, market reports, insurance, landlord-tenant laws, personal finance, urban development, economy, sustainability, and social issues. Nadia holds a B.S. in Business Management from Northeastern Illinois University in Chicago. You can connect with Nadia via email.

Nadia’s work and expertise have been quoted by major national and local media outlets, including CNN, CNBC, CBS News, Curbed, The NY Post, The Chicago Tribune, The Denver Post as well as industry publications, such as GlobeSt, Bisnow, Inman News, Multifamily Executive, and The Commercial Real Estate Show. Nadia also wrote for Multi-Housing News, Commercial Property Executive, HubSpot, and more. Prior to entering the real estate industry, Nadia worked in the legal field, where she gained over 10 years of experience in business, corporate, and real estate law.

Sign up for The Ready Renter newsletter

Get our free apartment hunting guide — plus tips, trends and research.

")

")

Related posts

Baltimore, MD vs. Washington, D.C.: Which city fits your renter budget?

Thinking about a move from Baltimore to Washington, D.C.? The nation’s capital has long been a magnet for renters chasing career opportunities and world-class culture,…

Miami vs. Los Angeles: A cost of living comparison for coast-hopping renters

Thinking about trading Miami’s tropical vibe for life in high-energy Los Angeles? Plenty of renters make the move each year. Miami has long been a…

Searching for apartments in late August: How to win the tail end of peak season

Searching for apartments at the end of peak season means moving fast, staying flexible and keeping your paperwork ready. Late-summer demand is still strong but…

Subscribe to

The Ready Renter newsletter