Office-to-apartment conversions break records again, with 90K rentals in the pipeline

Share this article:

Empty office buildings across the country are being reimagined as housing. Spaces once filled with desks and conference rooms are now being redesigned into rental apartments, giving new purpose to towers that no longer operate at full capacity.

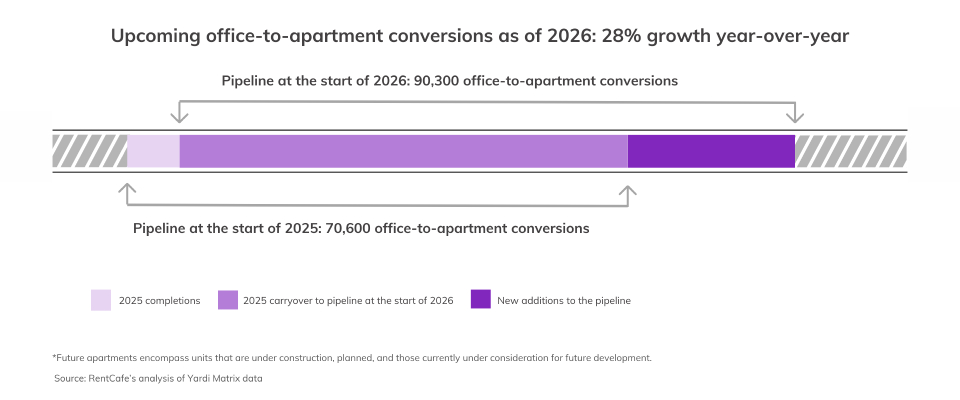

At the start of 2026, 90,300 apartments were in the process of conversion nationwide — up 28% from 70,600 a year earlier — marking another record year for office-to-apartment projects.

Key takeaways:

- The national office-to-apartment conversion pipeline reached 90,300 units at the start of 2026, up 28% year-over-year and nearly four times larger than in 2022.

- Office conversions now account for almost half (47%) of all future adaptive reuse projects nationwide.

- The New York metro area leads with 16,358 conversions in the backlog, followed by Washington, D.C. (8,479) and Chicago (4,360).

- Denver, Philadelphia and Cleveland are among this year’s newcomers in the top 10, ranking #6, #7 and #9, respectively.

The imbalance in the office sector didn’t emerge overnight. As Peter Kolaczynski, director of Yardi Research, explains, “COVID-19 is to the office market what e-commerce was to retail. As a result, there is simply too much office space in the market right now.”

In early 2025, national office vacancy was close to 20%, while physical occupancy in many buildings hovered around just 50%–55%. That gap has left millions of square feet underused, opening the door for large-scale residential conversions.

The shift is especially visible in major hubs like New York City, where older office buildings are moving through the conversion process even as parts of Manhattan’s office market grow busier again. The city added 143,000 residents in 2024 alone, intensifying the push to bring more housing into central neighborhoods.

Financial pressure and government-backed incentives are also accelerating conversions in 2026. With roughly one-third of U.S. office loans set to mature by 2027, many owners face mounting pressure to act on underperforming properties:

“A massive amount of office building loans — over $213 billion — are coming due by the end of 2026. When loans mature, borrowers need to either pay them off or refinance them. The problem is that many of these office buildings have lost significant value largely due to remote work trends reducing demand.”

Doug Ressler

Senior Analyst & Manager of Business Intelligence, Yardi Matrix

Despite growing interest, many office-to-apartment conversions take several years to complete. The process is often slowed by structural constraints, high construction costs, financing hurdles and local regulatory requirements.

A large share of today’s activity didn’t start this year. Nearly 66,500 projects already underway in early 2025 are still moving forward in 2026. When combined with newly proposed developments, they helped push the national total up by 19,600 units year over year — a reminder that conversions often unfold over multiple years.

Office buildings now represent the largest slice of adaptive reuse activity nationwide. In 2026, they account for 47% of all future adaptive reuse units — roughly 90,300 apartments out of 193,900 planned projects, up from 42% last year.

Hotels make up about 18% of future adaptive reuse projects, followed by industrial properties at 16%, while other building types — including healthcare facilities, schools, retail and government buildings — account for roughly 19%.

Share of future conversions by building category

47%

18%

16%

19%

The number of office-to-apartment conversions has expanded rapidly over the past four years. It grew from 23,100 units in 2022 to 45,200 in 2023, then climbed to 55,300 in 2024 and 70,700 in 2025, before reaching a new high of 90,300 units at the start of 2026.

What began as a response to excess office space is now a recurring feature of the housing landscape, particularly in dense cities where adding new supply can be difficult.

Future office-to-apartment conversions by year

45,200

The data shows future apartments from office conversions for each particular year. Data subject to change.

The types of office buildings being converted are also shifting. While newer offices built between the 1990s and 2010s make up just 2% of completed projects, they account for 6.4% of future conversions.

That figure now approaches the broader adaptive reuse market, where 7.4% of projects involve newer buildings — suggesting developers are increasingly willing to work with more modern office stock.

Nationally, more than 1.9 billion square feet of office space — or about 24% of total inventory — is considered suitable for conversion, according to the Conversion Feasibility Index (CFI) from CommercialEdge.

But eligibility doesn’t guarantee feasibility.

“Age matters, but so do footprint and structural layout. If a building is functionally obsolete as an office but has the right bones, it can be a strong conversion candidate.

Proximity to mass transit and walkability are key. Access to natural light is one of the biggest challenges in conversions — multiple exposures are often a must.”

Peter Kolaczynski

Director of Data & Research, Yardi

New York has largest office-to-apartment conversions pipeline, Denver and Philadelphia join top 10

New York is on track to convert the most former office buildings, with 16,358 rentals in the backlog. It is followed by Washington, D.C. (8,479 units) and Chicago (4,360), with Los Angeles (4,340) close behind.

Other large metros, including Dallas and Atlanta, also post strong slates of conversion projects. Meanwhile, Denver, Philadelphia, and Cleveland enter the top 10 this year, signaling broader geographic expansion.

Local governments are actively supporting conversions through incentives and regulatory changes. New York City has paired tax benefits with zoning reforms, while Washington, D.C., continues its Housing in Downtown initiative.

Elsewhere, Los Angeles and Boston have expanded adaptive reuse ordinances, while Minneapolis and San Francisco have streamlined approvals through code and permitting updates.

1. New York

- Future office-to-apartment conversions as of 2026: 16,358 units

- Share of office-to-apartment conversions as of 2026: 62%

- Office space suitable for residential conversion: 324.8 million square feet

The New York metro area leads the nation in office-to-apartment conversions after a 97% year-over-year increase, even as office occupancy has returned to pre-pandemic levels. Many older office buildings are still slated for conversion in 2026, driven by strong housing demand and layouts that are easier to adapt for residential use.

One notable example is 111 Wall Street, where more than 1500 apartments are planned as part of a large-scale conversion spanning roughly 1.1 million square feet. Projects of this scale highlight how older office buildings — particularly in Lower Manhattan — are being repositioned to meet housing demand without relying on new ground-up development.

2. Washington, D.C.

- Future office-to-apartment conversions as of 2026: 8,479 units

- Share of office-to-apartment conversions as of 2026: 64%

- Office space suitable for residential conversion: 125.1 million square feet

In Washington, D.C., the return of most government workers to in-person office work has increased demand for housing near the city’s core. As a result, converting existing office buildings has emerged as a practical way to add apartments in areas where new construction is limited.

A notable project is 450 5th Street NW, where a former office property totaling approximately 385,000 square feet is being redeveloped into around 500 apartments. The site sits just north of Pennsylvania Avenue and near key transit hubs, in a part of downtown Washington that many planners and officials are eager to transform into a more mixed-use, housing-friendly neighborhood as part of broader efforts to attract more residents back into the city center.

3. Chicago

- Future office-to-apartment conversions as of 2026: 4,360 units

- Share of office-to-apartment conversions as of 2026: 64%

- Office space suitable for residential conversion: 94.8 million square feet

Unlike the national trend, where future office-to-apartment projects are increasingly targeting newer buildings, Chicago’s conversion slate still leans heavily on much older office stock. Nationally, buildings slated for future conversions average about 72 years old, compared to 62 years for completed projects.

In the Chicago metro, however, future office-to-apartment conversions are expected to come from buildings averaging nearly 90 years old, underscoring how the city’s conversion activity remains concentrated in its historic downtown core.

A standout project is 105 West Adams Street, where roughly 400,000 square feet of underused office space is slated for redevelopment into 400 apartments. Notably, 30% of the units are planned as affordable housing for households earning around 60% of the area median income —adding new housing while reusing older office space in the Loop.

4. Los Angeles

- Future office-to-apartment conversions as of 2026: 4,340 units

- Share of office-to-apartment conversions as of 2026: 49%

- Office space suitable for residential conversion: 158.2 million square feet

In the Los Angeles metro, office-to-apartment conversions are increasingly viewed as a practical way to expand housing options while reactivating underused commercial space. A notable example is the former L.A. Superior Court Tower at 600 South Commonwealth Avenue, where a nearly 350,000-square-foot office building is slated to be redeveloped into 428 live/work apartments.

This project comes as Los Angeles has expanded its Citywide Adaptive Reuse Ordinance, broadening where and how office and other commercial buildings can be converted into housing and making approvals faster and more predictable across the city — a step officials see as essential to meeting the region’s housing goals.

5. Dallas

- Future office-to-apartment conversions as of 2026: 3,966 units

- Share of office-to-apartment conversions as of 2026: 82%

- Office space suitable for residential conversion: 49.1 million square feet

Office-to-apartment conversions continue to play a central role in adaptive reuse across the Dallas metro, where the wave of conversions has grown sharply year-over-year. A standout project is the redevelopment of the 14-acre Stemmons Towers campus, which is being transformed into Lumiére, a 394-unit upscale apartment community.

Large-scale projects like this highlight how Dallas is increasingly turning to office conversions to reposition aging commercial properties and add new housing across the metro.

6. Denver

- Future office-to-apartment conversions as of 2026: 2,991 units

- Share of office-to-apartment conversions as of 2026: 60%

- Office space suitable for residential conversion: 41 million square feet

Denver stands out this year after jumping from 15th place last year to one of the fastest-growing metros for office-to-apartment conversions. The shift is driven by a mix of local housing policies, growing affordability pressure, and a large stock of downtown offices that have struggled to recover, prompting the city to lean more heavily on conversions to add units without expanding outward.

A key example is the planned conversion of two downtown office towers at 621 and 633 17th Street, where more than 700 affordable apartments are set to be delivered — signaling a clear pivot toward using existing buildings to meet housing needs at scale.

7. Philadelphia

- Future office-to-apartment conversions as of 2026: 2,697 units

- Share of office-to-apartment conversions as of 2026: 45%

- Office space suitable for residential conversion: 52 million square feet

Philadelphia makes one of the biggest jumps in this year’s rankings after placing 18th last year, as office-to-apartment conversions gain traction in a city known for its historic building stock. With many downtown offices designated as landmark properties, conversions are often supported by preservation-focused incentives that allow buildings to be reused without altering their historic character.

A standout project is the redevelopment of the historic Wanamaker Building into a mixed-use destination with more than 600 apartments. This shows how Philadelphia is using conversions to add housing while keeping its architectural legacy intact.

8. Atlanta

- Future office-to-apartment conversions as of 2026: 2,642 units

- Share of office-to-apartment conversions as of 2026: 61%

- Office space suitable for residential conversion: 26.8 million square feet

Unlike many major cities, Atlanta is expanding office-to-apartment conversions outside its downtown core, tapping underused office parks and business districts. As a result, office conversions now make up over 60% of the metro’s adaptive reuse activity.

One example is the conversion of the office park at 2245 Northlake Parkway, which will deliver more than 200 apartments in a suburban business district, highlighting how Atlanta’s housing growth is extending beyond downtown.

9. Cleveland

- Future office-to-apartment conversions as of 2026: 1,771 units

- Share of office-to-apartment conversions as of 2026: 50%

- Office space suitable for residential conversion: 24.7 million square feet

Cleveland holds its place among the leading metros for office-to-apartment conversions after ranking 12th last year, supported by a steady flow of downtown redevelopment projects.

A notable example is The Rockefeller at 614 West Superior Avenue, where a 304,000-square-foot office building is slated for conversion into up to 436 apartments, helping bring more residents into Cleveland’s central business district.

10. Cincinnati

- Future office-to-apartment conversions as of 2026: 1,770 units

- Share of office-to-apartment conversions as of 2026: 62%

- Office space suitable for residential conversion: 18.2 million square feet

Cincinnati also relies heavily on office-to-apartment projects as a key driver of adaptive reuse across the metro. One project helping to shape that momentum is the redevelopment of Sky Central, a 380,000-square-foot mixed-use building that will introduce 281 apartments and penthouses, to downtown Cincinnati, strengthening the area’s residential presence.

Rounding out the top 20 metros are Charlotte, NC (#11 with 1,649 units); Bridgeport, CT (#12 with 1,565 units); Phoenix (#13 with 1,550 units); Detroit (#14 with 1,455 units); Minneapolis (#15 with 1,453 units); Kansas City, MO (#16 with 1,363 units); Milwaukee (#17 with 1,274 units); Jacksonville, FL (#18 with 1,268 units); St. Louis (#19 with 1,156 units); and Pittsburgh (#20 with 1,109 units).

Northeast leads the U.S. in office-to-apartment conversions

Conversions are no longer concentrated in just a handful of cities. The Northeast leads with 28,552 units, followed closely by the South at 26,527. The Midwest accounts for 19,945 conversions, while the West totals 15,300 projects.

The regional breakdown reflects deeper structural differences. In the Northeast, conversions are driven by a dense supply of older and very old office buildings, many constructed long before modern office layouts became the norm, making them easier to adapt for residential use.

The South’s rapid rise, meanwhile, mirrors a broader shift seen this year across apartment construction, where new development and redevelopment activity are increasingly concentrated in Southern metros. Faster population growth, expanding employment centers, and a growing stock of underperforming offices are pushing the South closer to parity with the Northeast — signaling a meaningful geographic shift in where office-to-apartment conversions are taking hold.

Three metros more than double their pipelines since last year

Some metros are scaling up at a remarkable pace. Philadelphia’s conversion total jumped 119% year over year, while Denver rose 114%, pushing both markets sharply up the rankings.

Metros with more than 100% y-o-y growth in office-to-apartment conversions

The data shows office-to-apartments currently under construction, planned or prospective. Data is subject to change.

Mid-sized metro areas are also showing sharp gains. St. Louis more than doubled its planned conversions, signaling that the trend is not limited to the largest cities.

Once financing, policy and viable buildings align, growth can accelerate quickly — even outside the country’s largest cities.

Office-to-apartment conversions exceed 50% of adaptive reuse projects in 12 top metros

In many metros, office conversions now drive most adaptive reuse activity. In 12 of the top 20 markets, they account for more than half of all projects. The trend is especially evident in large metros such as Washington, D.C. (64%), Chicago (64%), and New York (nearly 62%), underscoring the central role office conversions play in reshaping urban cores.

In Dallas and Minneapolis, office conversions make up about 82% of reuse activity, while Jacksonville and Phoenix exceed 70%, leaving little room for other building types in the redevelopment mix.

Despite broad national growth, not all metros moved in the same direction. In 2026, seven of the top 20 metros recorded year-over-year declines in their office-to-apartment conversion total — up from just three last year — pointing to a more uneven landscape.

Some pullbacks were modest. The Los Angeles metro dipped slightly, while Charlotte and Phoenix also saw small declines, suggesting pauses after periods of rapid expansion. Larger drops were more concentrated in specific markets, including Minneapolis (-22%), Kansas City (-19%), Pittsburgh (-11%), and Jacksonville (-11%). These declines highlight how local factors — such as financing constraints, zoning complexity, and shifting demand — are increasingly influencing which conversion projects move forward.

FAQs: Office-to-apartment conversions 2026

Q: How many office-to-apartment conversions are expected in 2026?

A: About 90,300 apartments are currently in the office-to-apartment pipeline.

Q: Which metro has the largest pipeline of office-to-apartment conversions?

A: The New York metro area ranks first with 16,358 units, followed by Washington, D.C. (8,479) and Chicago (4,360).

Q: How much of the adaptive reuse pipeline is made up of office conversions?

A: Office-to-apartment projects account for nearly 47% of all future adaptive reuse developments.

Q: Which metros are seeing the fastest growth in office-to-apartment conversions?

A: Philadelphia, Denver, and St. Louis have more than doubled their conversion count year-over-year.

Q: What’s driving the surge in office-to-apartment conversions?

A: High office vacancies, strong housing demand, and local incentives continue to fuel the trend.

Methodology

RentCafe.com is a nationwide apartment search website that enables renters to find apartments and houses for rent across the United States. This report was compiled by the RentCafe.com research team using apartment and commercial real estate data provided by our sister company, Yardi Matrix.

Adaptive reuse refers to the conversion of existing non-residential buildings into rental apartment communities. This analysis includes properties with 50 or more residential units.

Future office-to-apartment projects include developments that are currently under conversion, as well as planned and prospective redevelopments. Data is subject to change.

Completed projects are defined by Yardi Matrix as buildings that have received a certificate of occupancy and are ready for residents.

Projects under conversion refer to office buildings that are actively being redeveloped into residential properties but have not yet received a certificate of occupancy. Throughout this report, these may also be described as units in process of conversion, conversions underway, projects in development, or future office-to-apartment conversions.

Planned projects are engaged in the redevelopment approval process but have not yet begun construction.

Prospective projects carry a lower probability of completion and may still be in early design or feasibility stages, undergoing entitlement review, or temporarily placed on hold.

The share of office space considered suitable for residential conversion in each metro was calculated using the Conversion Feasibility Index (CFI) from CommercialEdge.

The CFI is a proprietary weighted scoring model developed by Yardi Research to assess the structural potential for converting office buildings into multifamily properties. It evaluates physical and locational characteristics such as building age, total square footage, floor plate depth, ceiling height, number of stories, primary use subtype, green certifications, walkability, transit accessibility, and whether a building is mid-block or on a corner. Each factor is weighted based on its importance to conversion feasibility, and buildings receive a composite CFI score.

Buildings are grouped into three tiers:

- Tier I (90–100 points): Top conversion candidates with highly favorable characteristics.

- Tier II (75–89 points): Quality candidates with strong potential but possible modification needs.

- Tier III (0–74 points): More challenging candidates requiring significant adjustments.

For this report, Tier I and Tier II buildings were used to estimate each metro’s pool of office space suitable for future conversion.

For the New York metro area, the CFI analysis includes office buildings across Manhattan, Brooklyn, Queens, the Bronx, and Staten Island.

This report has been updated on April 2nd, 2026, to revise figures related to office space suitable for conversion.

Fair use and redistribution

We encourage you and freely grant you permission to reuse, host, or repost the research, graphics, and images presented in this article. When doing so, we ask that you credit our research by linking to RentCafe.com or this page, so that your readers can learn more about this project, the research behind it and its methodology. For more in-depth, customized data, please contact us at media@rentcafe.com.

Share this article:

Florin Petrut

Florin Petrut is a real estate writer and research analyst with RentCafe, using his experience as a social media specialist and love for storytelling to create insightful reports and studies on the rental market. With a strong interest in the renter experience, he develops data-driven resources that explore cost of living, affordable neighborhoods, and housing trends, helping renters make informed decisions about where and how they live. Florin holds a B.A. in Journalism and an M.A. in Digital Media and Game Studies.

Sign up for The Ready Renter newsletter

Get our free apartment hunting guide — plus tips, trends and research.

")

")

Related posts

Your first month of solo apartment life: A week-by-week guide for new renters

Moving into your own apartment is one of the most exciting milestones of young adulthood. But it’s also one of the most overwhelming. Between setting…

5 questions to ask before renting an apartment in Asheville, NC

Asheville has earned its reputation for good reason. The food scene punches well above its weight, the Blue Ridge Mountains are a short drive away…

June 2026 self storage report: Rents slip 1.5% annually, edge up 0.7% from May

National street rates averaged $135 in June 2026, down 1.5% year-over-year but up 0.7% from May, as the summer moving season provides a modest seasonal…

Subscribe to

The Ready Renter newsletter