Share this article:

Our recent report on the profile of renters today revealed an 82% increase in high-earner renters between 2015 and 2020. This percentage is significantly higher than the rise in overall renters, which was just 3% during the same timeframe. The number of people who could afford to buy but choose to rent reached 2.6 million, and among them, over 3,000 have an income of over $1 million.

So, what makes millionaires want to be renters? We turned to expert professors in the fields of finance, economics and real estate to gain some insight.

Why do so many high-income earners turn to renting instead of buying? Why is homeownership not a priority for them?

- Balbinder Singh Gill, Assistant Professor of Finance and Sustainability, School of Business at Stevens Institute of Technology

There are two important possible explanations for why so many high-income earners are turning to renting. The interest charged on the requested mortgage loan amount is the first one. Banks increase the interest rate on mortgage loans during periods of high inflation to deter people from borrowing for potential property purchases. This is because inflation can change the value of money over time.

Due to an anticipated decline in inflation over time, lenders would charge a higher interest rate to protect themselves against a probable loss of value of the mortgage loan amount towards the end of the loan’s specified term compared to the value of the same mortgage loan amount when the mortgage loan was first originated. Furthermore, those with high incomes are more likely to buy large residences, usually sold at higher prices.

Prospective buyers must request higher mortgage loans to purchase these properties. As these mortgage loans provide a greater risk to the mortgage lender, they frequently have higher interest rates.

The state and local property taxes is the second explanation. Owners of larger sized properties pay higher local and state property taxes. Before the repeal of the State and Local Tax (SALT) cap deduction by the 2017 Tax Cuts and Job Act (TCJA), taxpayers were able to fully deduct their locally paid property taxes in their federal tax returns.

After the repeal, taxpayers are only allowed to deduct a maximum of $10,000 paid state and local taxes from their federally taxable income per year through 2025. The SALT cap deduction repeal will hurt more higher-income taxpayers with higher marginal tax rates in States with higher local and state property taxes such as New York, New Jersey, Connecticut, California, and Maryland.

- Brent Smith, Professor and CoStar Group Endowed Chair in Real Estate Analytics, The Virginia Commonwealth University School of Business

Many high earners are also empty nesters or generally without young children, with both free cash flow and free time. They seek flexibility in lifestyle. Renting allows for increased mobility. Today’s high earners change jobs at an increasing rate and significantly more than in previous decades.

Although the average annual returns to homeownership have been high in recent years the average return over the last +/- 100 years is 5%, and that return is dependent on a constant stream of investment in repairs and maintenance to stave off depreciation.

A significant number of w-2 earners now are unable to itemize deductions after the “Tax and Jobs Act of 2017.” Thus, the incentives to invest in housing are reduced through the loss of mortgage interest deduction.

- Cephas Naanwaab, Associate Professor of Economics, Willie A. Deese College of Business and Economics at North Carolina Agricultural and Technical State University

There are several factors that explain the rise in high-income renters: rising home prices, declining tax incentives, lack of willingness to relocate, and student loan debts. Home prices remains the major factor determining homeownership, and we have seen that overall, housing affordability has been declining for decades, not only for the middle class, but for high-income earners as well.

The S&P CoreLogic Case-Shiller National Home Price Index shows that between 2015 and 2020, home prices increased 29% nationally. In the high-cost, large metro areas of the West Coast and Northeast, home prices accelerated even higher than the national average. The mismatch between supply and demand for housing continues to fuel rising prices. As home prices have increased over the years, and the tax benefits of ownership, particularly on the high-end of the market have declined, would-be buyers have naturally gravitated to renting.

The share of cost-burdened American households—those that spend more than 30% of their household income on housing—has reached the highest it has ever been (Joint Center for Housing Studies at Harvard University). Even if high home price is not a deterrent, the indirect cost of homeownership, such as HOA fees, home maintenance, property taxes, and insurance costs have also been on the rise. These considerations, coupled with high student loan debts, are enough to deter high-income buyers from owning, preferring instead to rent and not have to deal with all these other challenges that come with ownership.

A second plausible cause of the increase in high-income renters is the declining tax incentives to own a home. In 2017 Congress passed the tax reform known as “Tax Cuts and Jobs Act”, which scaled back tax incentives that hitherto benefited high mortgage homeowners in high-property tax states. Under the new law, which took effect January 2018, state and local property tax deductions (SALT) were capped at $10,000. The legislation also capped deductible mortgage interest on mortgage debt at $750,000.

For example, a homebuyer in New York City looking to buy a $2 million house would be on the hook for a property tax bill of $25 – $30,000 but can only deduct $10,000. Plus, mortgage interest deduction on that loan will be capped at $750,000. In essence, the new law disincentivized home buyers in high-property tax states, particularly those looking to buy high end properties. For high-income earners located in more expensive coastal cities of the Northeast and West Coast, which coincidentally are also high-property tax jurisdictions, the unintended consequence (or intended, depending on which side of the isle you belong), of the new law was to deter many would-be homes buyers.

- Russell Spears, Assistant Professor of Economics, Department of Economics, Finance and Quantitative Analysis in Kennesaw State University’s Michael J. Coles College of Business

To understand the logic behind the high-income earners ($150,000+ annually) who make up most of the renting behaviors, it is important to focus on two key components: costs and time. First, we can address the cumbersome costs to home-buying in addition to the simple list price of the home. The home-buying process tends to take several months to a year on average, even buying sight-unseen. According to Nelson (2022), prior to even making an offer on a home there are multiple steps: pre-qualification (which takes 8-10 days), home search (4-5 months), constructing an official offer (5 days).

At this snapshot point, the consumer is already months into the process, making it difficult and costly to pivot to renting when considering time costs and credit hard hits. It is now important to complete the process contingent upon the seller’s acceptance of the offer, namely mortgage acquisition (21 days minimum) and closing process (40-50 days).

So now, the consumer is most definitely at a point of no return, as he or she is simply thousands of dollars invested with costs that renting doesn’t require. For example, a $500,000 home purchase requires earnest money which is typically 1-3% of the sales price (Chism, 2023). If we take the lower end of this estimate, the homebuyer must provide $5,000 in earnest money generally via cashier’s check or wire. Also, the home buyer generally is advised to order an inspection, which could range between $350-$500 depending on the state.

In addition, depending on the negotiations, the buyer must have the required cash-to-close, which includes the total closing costs minus any fees that are rolled into the loan amount. For example, using the $500,000 abovementioned home, given a 5% down payment, one must bring at least $25,000 to closing – but often these funds must clear PRIOR to closing.

Other costs related to home-buying include HOA fees, utility set-up/installation, and other costs that vary depending on location, such as property taxes and homeowner’s insurance, which are often rolled into escrow. Again, costs and time are key considerations to home purchases, as high-income earners may not see home buying as worth the time and money when, on average, renting involves significantly less time and costs.

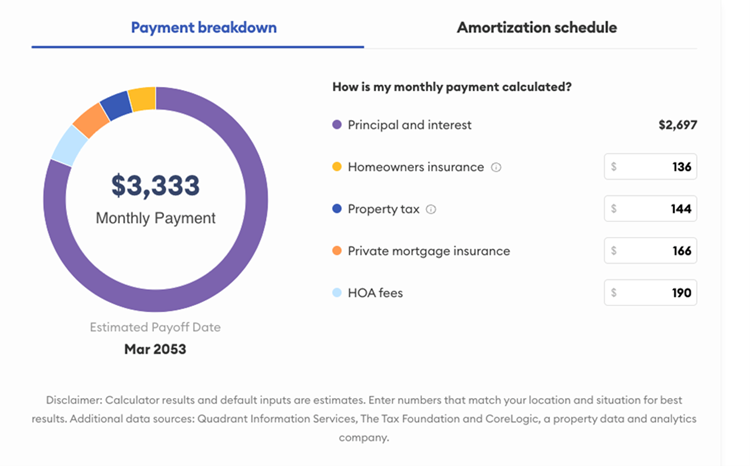

For example, let’s consider purchasing a home in Atlanta versus renting a comparable apartment with the same number of bedrooms but slightly less square footage. On average, again with comparable observations, rental payments for 1-year leases are 28% less than mortgage payments. Using Forbes’ (2023) general Georgia Mortgage Calculator, which consistently reports a low-end estimate, our $500,000 home with the given variables would require a $3,333 mortgage payment (Figure A).

Whereas a condo or apartment, comparable by bedroom, bathroom, and area, averages just under $2,600 per month, not including rent specials.

It is important to note, though, that this elevated payment can be accredited to the swelling housing market since 2020. In addition to this cost difference, the renter is not married to a 30-year loan, where building any considerable equity could take years.

- Scott L. Baier, Professor and Department Chair, John E. Walker Department of Economics, Wilbur O. and Ann Powers College of Business

Several factors have likely come into play that have impacted the choice of renting versus buying. On the demand side, individuals are waiting longer to have families and so they may not want the 2500 square foot house in the suburbs. Instead, they may prefer to live in the cities where they may be closer to work and can enjoy more of the amenities large cities have to offer. In addition, on the supply side, the construction of new homes was slow to rebound following the great financial crisis of 2007-2008. This has resulted in an increase in the average price of homes and has caused some to turn to renting instead of buying.

- Sourav Batabyal, Ph.D., Assistant Professor of Economics, Department of Finance and Economics, Wall College of Business Administration at Coastal Carolina University

Owning a home may not be ideal for everyone, and renting does have its benefits, too. In contrast to homeowners, renters do not incur maintenance or repair expenses. On the other hand, all costs associated with home upkeep, remodeling, and renovation fall under the purview of the homeowner.

Many midscale to affluent apartment complexes include amenities like a fitness center or pool as standard features at no extra cost to renters. These luxuries would probably cost a homeowner thousands of dollars to install and maintain if they wanted to use them. Condo owners are not excluded from these expenses either.

These costs are incorporated into their monthly homeowners’ association (HOA) fees. Renters don’t have to pay property taxes, whereas homeowners may face a considerable financial burden from real estate taxes, which differ by location. The amount of property taxes you pay can change depending on whether property values increase or decrease over the course of the economic cycle. Renters are unaffected by a rise in property taxes, but homeowners are.

Renters often pay an upfront fee that is typically equal to one month’s rent as a fully refundable security deposit (assuming there is no damage). When getting a mortgage to buy a house, a buyer must have a significant down payment, typically 10%-20% of the purchase price of the house. Renting is a preferable option for someone who doesn’t want to spend a sizable down payment.

At the end of their lease period, renters have the choice to downsize into less expensive living spaces. This kind of adaptability is crucial for retirees who want a less expensive, more affordable choice. If a homeowner already spent a lot of money on home improvements, the sale price might not be enough to cover these expenses, making it considerably more difficult to sell and move. Similar to homeowners with fixed-rate mortgages, the amount of monthly rent is normally fixed during the contract period. This helps consumers to budget more efficiently as they know the amount of monthly payment they are required to pay. But adjustable-rate mortgages (ARMs) can fluctuate, often resulting in rising mortgage payments due to higher interest charges.

- Xiaozhou Ding, Assistant Professor of Economics at Dickinson College, an expert on labor and urban economics

In recent decades, there has been a new phenomenon in the U.S. in what we called urban revival (or urban gentrification). This is the trend where high-income earners are actually moving back to urban centers, in contrast to the times before 1980s that people moved to suburban areas in the U.S. The driving force of this trend is the ‘rising value of time’ (see Yichen Su 2022) that attracts people to reduce commuting time and work longer.

There is also a trend of highly skilled people (who also tend to be high-income earners) to move into bigger and smarter cities (cities with more highly skilled workers), while the skill-wage premium in the U.S. has been widening (see Rebecca Diamond 2016). Taking these patterns into consideration, more high-income people choose to rent instead of owning a home probably because housing supply in urban centers is lower compared to suburbs.

What makes those who can afford to buy turn to renting? Is the main reason price, or are there other factors at play, such as location, cultural shift, flexibility to move around for their career, investment considerations, etc.?

- Cephas Naanwaab, Associate Professor of Economics, Willie A. Deese College of Business and Economics at North Carolina Agricultural and Technical State University

Price remains the major factor when considering homeownership. However, other costs of owning weigh heavily on potential buyers: maintenance/repairs costs, property taxes, HOA fees, insurance etc. The allure of homeownership as an investment appears to be waning. In the aftermath of the housing bubble crash of 2007-08 and the ensuing Great Recession, speculative homeownership for investment purposes has less appeal among many. If the goal of homeownership is investment, then other better alternative investment tools offer higher returns and that could shift demand for ownership.

Additionally, a generational shift in homeownership appears to be playing out, as homeownership rates are lower among millennials than Gen Xers and Baby Boomers. According to Census Bureau data, around 37% of millennials own their home— a figure that is eight percentage points lower than that of Gen Xers and Baby Boomers at the same age. Furthermore, as the RentCafe study shows, more millennial millionaires are choosing to rent compared to Gen X and Baby Boomers.

A third, albeit minor cause of rising high-income renters is job considerations. Some high-income earners prefer to rent rather than be tethered to a particular location because of a home. The ease of being able to change jobs easily and move on a whim is an allure that some can’t resist.

- Reid Cummings, Interim Assistant Dean for Financial Affairs, Mitchell College of Business, Associate Professor of Finance and Real Estate, University of South Alabama

Although price is certainly a factor (both purchase price and the cost of a mortgage), for many, maintaining the flexibility of being able to quickly relocate — should a job change or a family situation require it — is appealing.

- Russell Spears, Assistant Professor of Economics, Department of Economics, Finance and Quantitative Analysis in Kennesaw State University’s Michael J. Coles College of Business

The affordability index for home-buying has remained strong due to wage and credit score increases (Equifax, 2023). However, affordability doesn’t necessarily drive consumption, as we’ve seen in these data of renters versus buyers. When surveying consumers on the topic of home-buying versus renting, it was confirmed by Gallup (2023) that price is one variable of many. It is here that it is important to mention the importance of the gig economy.

According to Statista (2023), the gig economy is a section of the economy which consists of independent contractors and freelancers who perform temporary, flexible jobs. This can be cross-referenced to the Bureau of Labor Statistics’ (BLS) definition of a contingent worker which includes freelancers, independent contractors, consultants, and other non-permanent workers who are hired on a per-project basis (BLS, 2023).

The national survey of gig workers reported a market size value of $355 billion, which is expected to increase to $873 billion by 2028 (EPI, 2023). These estimates make a strong case for the “flexibility to move around” factor when considering renting versus owning.

An interesting statistic reported by Realtor.com (2023) found that 1 in 5 home purchases were by investors who do not plan on living at the residence. Interpreting this 20% investor composition of home-buying can be translated, in part, to investment considerations being a factor of less home-buying and more renting. While cultural shifts, location, and investment opportunities could be noisy factors, the emergence of the gig economy could have a strong effect on the shift to high-income renters.

- Scott L. Baier, Professor and Department Chair, John E. Walker Department of Economics, Wilbur O. and Ann Powers College of Business

Price is always going to be a factor, but other factors are important as well. Location will also be a driver. Where individuals choose to live will depend on how close they are to their work and how close they are to things they enjoy doing at their leisure. Another factor may be time. Some individuals may not want to spend time and money on the upkeep of a house; as renters, someone may do some of the upkeep for them. Finally, family size may impact the decision to rent versus buy. People who are single or living together without children may not need the space, and renting could be a better option for them.

Are there financial or tax benefits to renting even when you can afford to buy a home?

- Balbinder Singh Gill, Assistant Professor of Finance and Sustainability, School of Business at Stevens Institute of Technology

Yes, if you decide to rent over owning a property then you are not required to pay (1) maintenance costs or repair costs, (2) real estate taxes, (3) down payment for the purchase of the property, and (4) purchasing costs. Moreover, some cities have rent controls which keep the rents affordable.

- Russell Spears, Assistant Professor of Economics, Department of Economics, Finance and Quantitative Analysis in Kennesaw State University’s Michael J. Coles College of Business

According to the Gallup (2023) survey, tax benefits were a consideration of owning a home. I have presented evidence of financial benefits to renting, but tax benefits only apply to home buying. However, it is extremely important to remember the property taxes paid on the home versus the tax benefit you could receive from being a homeowner.

According to Forbes (2022), the Internal Revenue Services (IRS) allows for common tax breaks that include: mortgage interest deductions, real estate taxes deduction, rate points deductions, private mortgage insurance deductions, moving expenses deductions, and various tax credits that could help your marginal tax rate. Depending on your filing status and itemization, you could net up from deductions compared to your property tax expense as your marginal tax rate could be lower when taxable income is reduced.

The terms for tax deductions in renting are far more stringent. According to Tax Slayer (2023), there are multiple qualifications that must be met to qualify for limited tax deductions such as residential status, tax filing status, and proof of taxes paid. So, the tax benefit appeal would not be the dangling fruit for the renter, but simply the analyzed cost savings per month.

- Scott L. Baier, Professor and Department Chair, John E. Walker Department of Economics, Wilbur O. and Ann Powers College of Business

There are some financial benefits to renting. The most obvious benefit is that the renter does not have to pay property taxes. Aside from that, there are other financial benefits that the renter may incur. The renter may not have to pay for or spend time with upkeeping the yard or the property. They may not have to pay for water services, sewer services, or other utilities. While some of these may be factored into the rental price, it may be more convenient for the renter to pay for all of these services as part of their rent.

- Sourav Batabyal, Ph.D., Assistant Professor of Economics, Department of Finance and Economics, Wall College of Business Administration

You cannot deduct residential rent payments on your federal income taxes. You might be allowed to deduct some of your rent from your state income taxes depending on which state you live in. For example, in California, if you pay rent for at least half of the year and make less than $49,220 for single filers or $98,440 for married filers, head of household, or qualified widower, you may qualify for a tax credit for $60 to $120.

If a taxpayer uses rented or leased property for both personal and business purposes, you may only deduct the portion used exclusively for your business. If you are self-employed and utilize a specific area of your house for your business, you could be able to claim the home office deduction provided you reside in a state that permits this practice.

If your lease agreement states that you pay property taxes as part of the terms of rent, you can deduct or receive a credit for that portion of your rent if you live in a state where this practice is legal. Additionally, even renters qualify to deduct some property losses or damages incurred as a result of federally declared disaster after your insurance payouts.

When considering the return on investment of a home, how does it compare to other types of investments?

- Balbinder Singh Gill, Assistant Professor of Finance and Sustainability, School of Business at Stevens Institute of Technology

The return of investment on a home is the profit earned from the purchase of the home after the deduction of costs incurred of owning the home. Homeownership costs include the purchasing price and any additional expenses associated with repairs or remodeling. The return on investment is only realized after the sale of the home, and it is higher when you decide to own the property for a longer period.

For example, if we decide to keep a home for 10 years then the return on investment of a home should be higher than the S&P 500 stock market average yearly return for the last 10 years, as of the end of February 2023. We assume that dividends are reinvested, and returns are adjusted for inflation, then the S&P 500 stock market average return was 9.57%. The return on your home investment should be higher than 9.57% if you decide to keep your home for at least 10 years.

- Cephas Naanwaab, Associate Professor of Economics, Willie A. Deese College of Business and Economics at North Carolina Agricultural and Technical State University

The question one should really ask is whether a home is an investment or a residence? For most people, it is both, which complicates making comparisons between homeownership as an investment with other forms of financial investments. That said, suppose that a homeowner is paying $1500 per month in mortgage and other associated costs of homeownership, and they could be renting a similar place for $1500, the benefit of ownership over renting is the home value appreciation. But then, a homebuyer typically must put down 20% which if they choose to rent can be put into other investments.

Thus, the forgone returns on the downpayment had they chosen to rent and then invest it in alternative assets could in the long run offset the benefits that come from home value appreciation. This however assumes that the renter had the discipline and the will to invest the downpayment in a well-diversified portfolio such as an S&P 500 index fund or ETF. They probably could have had a better return, based on historical returns of the S&P 500, than investing in a home.

The yearly average returns on the S&P 500 has topped 10% over the last 30 years. During the same time, the average return on real estate, as measured by home price appreciation has been 3-4% per year. Adjusted for inflation, the average return on a diversified investment like the S&P 500 easily outperforms the average returns on real estate.

- Russell Spears, Assistant Professor of Economics, Department of Economics, Finance and Quantitative Analysis in Kennesaw State University’s Michael J. Coles College of Business

It is important to understand the basics of wealth management: diversification. Investment portfolio balance varies across the investor group, but it is important to mention that most portfolios are composed of property/real estate. Most former financial advisors like myself promoted a general rule of thumb that real estate allocation in an investment portfolio should safely average between 5% and 10%.

Real Estate Investment Trusts (REITs) are traded daily in the market, and it is generally advised to add these financial derivatives to a portfolio as a way of diversification. Again, the average investor cannot afford multiple properties, but any properties that are owned are considered an annuity, which relies on guaranteed revenue streams – i.e., rent. It is also important to remember if you sell an investment property, you are subject to an additional realized gains tax. The return on an investment of a home strictly depends on the price paid and the market itself.

It is difficult to forecast the length of a booming housing market with the conflicting factors of low inventory and increasing interest rates. So, when considering a return on investment of a home, there is a litany of other, better investment opportunities which is why portfolio management calls for only a 5%-10% REIT composition. It is also important to note the time to build equity on a traditional, 30-year mortgage, which again, could only benefit the homeowner if the market doesn’t change course.

Why are some major urban areas turning into millionaire renter hotspots?

- Cephas Naanwaab, Associate Professor of Economics, Willie A. Deese College of Business and Economics at North Carolina Agricultural and Technical State University

First of all, major urban areas have a higher concentration of millionaires compared to smaller urban or rural areas. There are more than a million millionaires in New York City alone. So, to the extent that there are any millionaire renters at all, they are more likely to be found in major urban areas. It is no surprise that New York has the highest number of millionaire renters.

Second of all, the major urban areas typically have higher home prices and higher property taxes. As home prices increased over the years, the type of houses millionaire households would typically buy have seen their prices increase too. Couple together higher home prices and higher property taxes, with the tax reform of 2017 capping property tax and interest deductions, the cost of owning expensive properties deters millionaires away from owning to renting.

- Reid Cummings, Interim Assistant Dean for Financial Affairs, Mitchell College of Business, Associate Professor of Finance and Real Estate, University of South Alabama

My answer to this question is a bit anecdotal. My daughter and son-in-law are 27 and 31, respectively. Both high earners, they met while working in Washington, D.C. but during the pandemic, they decided to move to Dallas. To be sure, Dallas-Fort Worth is certainly an urban area with many of the amenities one would expect in a major city. But after two years, they decided to move back to D.C.

The reason was simple: even though they could do many of the same things in Dallas as in D.C., in Dallas, they had to drive 20 or 30 minutes on a 6-lane highway to get where they wanted to go. In D.C. though, they simply have to walk a few blocks, hop on the Metro, and within minutes, they are easily across town. Although they are renting in D.C and may buy one day, for now, they are loving their care-free renters’ life in one of the country’s most amazing cities.

- Russell Spears, Assistant Professor of Economics, Department of Economics, Finance and Quantitative Analysis in Kennesaw State University’s Michael J. Coles College of Business

While San Francisco saw the most significant increase in “millionaire renters” from 2015-2020 among major urban cities, Seattle’s tripling of high-income renters makes it the nation’s fastest-growing area for affluent renters (RentCafe 2023). Matrix (2023) added that this rise could be due to convenience and security preferences, as the lure to mid-rise to high-rise buildings with concierge services add appeal. Furthermore, as mentioned before, it is the flexibility over restriction to movement.

Overall, urban areas see more income inequality, which forces us to look at households earning less than $50,000 per year. According to Capps (2023), this group of renters fell 11% as poorer renters moved in with family members. From a purely speculative perspective, high-income owners could be temporarily renting until the housing market cools and inventory stabilizes, providing a better investment opportunity. If the cost of money continues to rise via interest rate hikes and credit begins to tighten, we may see a shift in renting demographics.

- Scott L. Baier, Professor and Department Chair, John E. Walker Department of Economics, Wilbur O. and Ann Powers College of Business

In addition to a robust labor market, some urban areas are turning into rental hotspots because of the cultural amenities and active social life that those areas provide. Many of these urban areas have not added much to the housing inventory, so the supply does not match the increased demand for rental units.

Share this article:

Mihaela Buzec

Mihaela Buzec is a senior writer, researcher, and online content developer for RentCafe, where she has over 7 years of experience writing about the real estate industry. She authors important resources such as the statistics pages describing generational patterns and renter's guides that help renters in their journey. Her work has appeared in publications such as Apartment Therapy, Indy Star, and Investopedia.

Mihaela is a published researcher and activates within academia as well. She holds a BA in English and German Language and Literature, an MA in Current Linguistics, and a PhD in neurolinguistics.

Sign up for The Ready Renter newsletter

Get our free apartment hunting guide — plus tips, trends, and research.

")

")

Related posts

Chicago vs. Boston: The cost of living breakdown every renter needs to know

Chicago or Boston? For a lot of renters searching for apartments, the choice comes down to fit, which city matches the life you’re after and…

A renter’s guide to public transit in Trenton, NJ, and getting around without a car

Trenton sits at an unusual crossroads. New Jersey‘s capital is one of the few cities in the country where you can catch a train north…

5 questions to ask before renting an apartment in McAllen, TX

McAllen has a lot going for it as a place to settle down for renters. The cost of living is low, the food is outstanding,…

Subscribe to

The Ready Renter newsletter